January 30, 2023

2023 Investment Outlook

Executive Summary

- Stocks entered their first bear market since 2009 as persistent inflation, aggressive central bank steps to tighten monetary policy, and a slowing U.S. economy caused markets to reset valuations.

- The year saw steady increases in interest rate expectations as the Fed Funds rate ended 2022 at 4.50%. The bond market was equally as volatile as stocks; fixed-income assets coped with accelerating inflation and a Federal Reserve struggling to catch up to restore price stability.

- By the end of 2022, while inflation has likely peaked, both stocks and bonds face the push-pull of economic positives (normalizing price trends, slowing pace of Federal Reserve actions) and negatives (late economic cycle, sluggish earnings growth, continued weakness from higher interest rates and inflation).

- We continue to underweight equities in our portfolios relative to their asset class targets. We also continue to favor value equities, though we prefer mid and small-cap companies now more than in 2022. Large-cap value stocks were the beneficiaries of investment flows from growth stocks last year. As a result, we see almost all large-cap U.S. equities as either expensive or no better than fairly valued. We see better return opportunities in foreign equities and improved price trends in these markets.

- We continue to selectively use alternative asset classes to reduce portfolio risk. These assets did an exceptional job in 2022. While they may not provide the same level of outperformance this year, we are not ready to shift to a more aggressive portfolio stance yet.

- We were very concerned last year about future expected returns, but the difficult conditions of 2022 make us more positive on the long-term outlook for investors today. Cash and fixed income can finally expect returns near historical norms for the first time in over a decade. Equity investors should also expect higher returns as valuations continue to normalize. However, 2022 showed many of the characteristics of a classic bear market, with several violent rallies and false starts to a new bull market. We expect this pattern to continue in 2023; we will selectively look to add risk but do not think the stock market has fully discounted a moderate or prolonged recessionary outcome. We still expect the bear market is in place in the U.S. and will look for more evidence that economic conditions or valuations justify shifting tactics.

Introduction

While many speculative stocks began to weaken in late 2021, the most followed U.S. benchmark, the Standard & Poor’s 500 Index, actually peaked on the second trading day of 2022 (January 4). The S&P entered a bear market in mid-June, closing 20% off the all-time high reached five months earlier. While most of the damage in stocks occurred in the first half of 2022, there was continued weakness in the second half bookended by two sharp rallies, one from mid-June to early August and another from mid-October to late November.

In the bond market, the placid conditions of recent years were shaken by the Federal Reserve’s steadily more hawkish rhetoric. The yield on the 10 Year Treasury bond, which began the year at about 1.5%, raced to over 3% by May and peaked at over 4% by October. The bond market struggled to keep up with a series of progressively worse-than-expected inflation readings; across the globe, central banks piled on top of one another to address their own inflationary challenges with tighter monetary policy.

Market Overview

The story of 2022 was an economy and market finding bills coming due for past choices (or sins, depending on your perspective). The most obvious culprit was inflation, which we addressed in both our 2021 and 2022 outlooks. The primary causes and assignments of the blame for last year’s inflation will be studied well into the future. Whether it was the aggressive fiscal and monetary stimulus, an economy recovering from the pandemic much faster than expected, lingering supply chain bottlenecks, or a Federal Reserve that was much too late to cut off support and money printing, it’s easy to find a litany of reasons why inflation reared its head in 2022. The Consumer Price Index peaked in June at an annualized rate of 9.1%. It started to gradually decline in the second half of the year, finishing December at 6.5%. Its glide path in 2023 will likely be one of the key market movers in the first half of the new year and perhaps beyond.

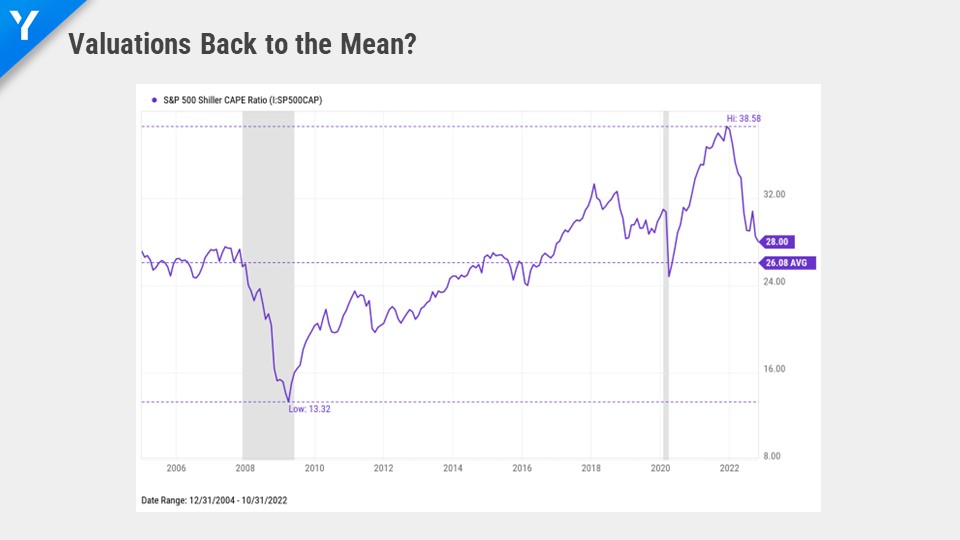

The other primary effect of the 2022 market was a revaluation of almost all asset classes. Since the Great Recession, lower trend growth, low inflation, or almost constant intervention from central banks kept interest rates at levels that allowed stocks to trade at historically high valuations. As the bond market repriced a new regime of Federal Reserve policy, suddenly there was an alternative to stocks again. The Fed started slowly with a 0.25% hike in March, but the constant drumbeat of inflationary headlines forced a 0.50% move in May and then four 0.75% increases during mid-2022 followed by a final 0.50% salvo in December. Fixed income, and by late in the year, even money market funds and bank deposits offered returns not seen in over a decade. Stocks followed suit by adjusting valuations to price higher expected future returns in the form of lower price-to-earnings (P/E) ratios. The most dramatic moves were seen in growth stocks, particularly technology sector companies with little to no earnings, as investors demanded more predictable valuations in a world where 3 and 4% returns could be had risk-free.

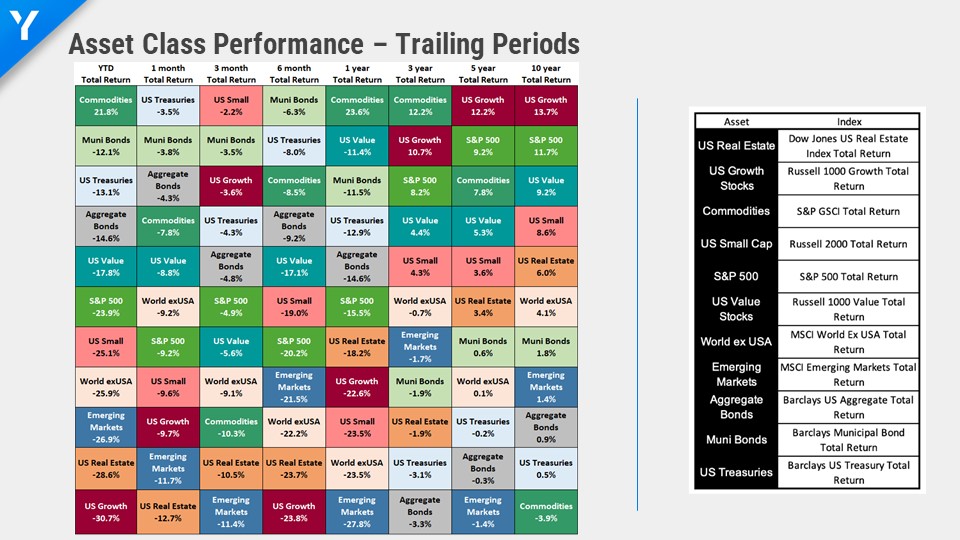

The S&P 500 ended the year down 18.1% in 2022. While the S&P represented a cross-section of all U.S. stocks, there was a significant churn underneath the surface between growth and value stocks. Two of the other commonly referenced U.S. benchmarks told the story. The old economy Dow Jones Industrial Average, tilted toward large companies with safe, predictable earnings and lower valuations, was down only 6.9%. The technology heavy NASDAQ, which had ballooned in recent years with the stunning performance of several mega-sized companies and many other smaller rapidly growing companies with less earnings predictability, was down 32.5%! 2022 represented one of the sharpest style reversals from growth to value stocks ever seen in a single year.

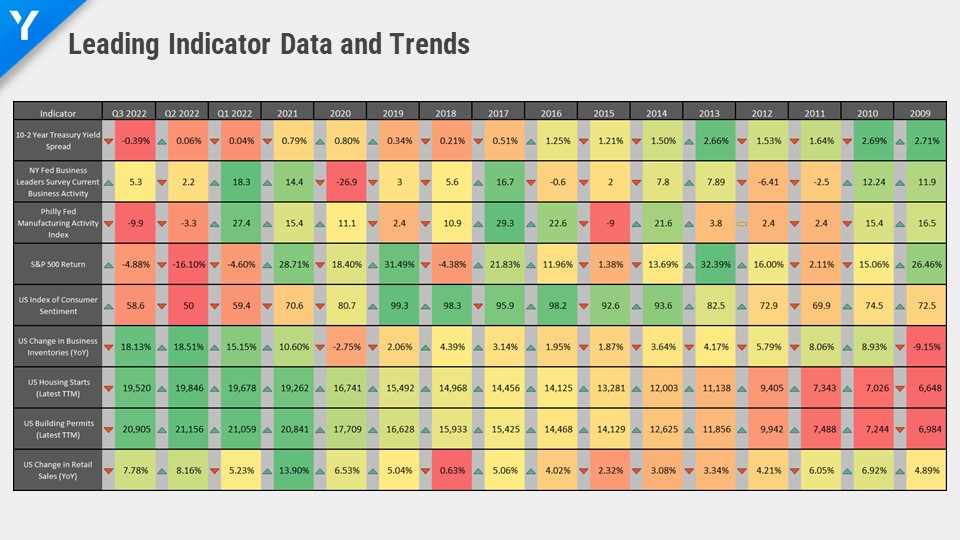

With the difficult conditions of 2022 (high inflation, higher interest rates, lower stock prices), it would be logical to expect the U.S. economy to show obvious signs of cracking. However, it remained largely resilient through the end of the year. There are no immediate signs of recession with Fed growth estimates for Q1 2023 appearing solidly positive. Although there are signs that many of the economic challenges have been pushed deeper into 2023 or even 2024 rather than eliminated, the labor market has made the future path of interest rates uncertain heading into a new year. The unemployment rate ended the year at 3.5% and while jobless claims have inched higher and layoff announcements are scattered through corporate America, there has not been enough pain in the job market to force the Fed’s hand to pause current policy or pivot course…yet. The strength in jobs and sticky wage inflation may be a reason why the Federal Reserve will keep interest rates higher for longer in 2023.

After a stellar 2021 and solid 2022, corporate earnings estimates are coming down for 2023. Q4 2022 earnings estimates dropped almost 7% over the course of the quarter, and there is a wide dispersion of outcomes for full-year 2023 estimates, with some Wall Street strategists forecasting levels 10-15% below current consensus. Keep in mind that most of the damage to stock markets in 2022 was from valuation compression; if there is a recession, whether economic or in corporate earnings only, there could be a second leg lower to stocks in 2023.

After two brief but fierce stock rallies in 2022 fueled by hopes that the Federal Reserve might be winding down or reversing its prescriptions of rate hikes, central bankers have pushed back strongly on rate cuts in 2023 in order to avoid renewed risk-taking and easy monetary conditions. A key faceoff this year will be between the Fed and the markets; the bond market is already forecasting rate cuts to begin late in 2023. Meanwhile, the Fed continues its monthly quantitative tightening program of removing $95 billion in cash from the economy through ending new Treasury and mortgage-backed security purchases. The dip in the money supply is likely a key factor in the drop in risky stocks and speculative assets.

While inflation is on the wane, it also remains to be seen if it will dip back toward the Fed’s preferred 2% level at the same pace as its drop from the June peak to current levels. There remain several components of inflation in services sectors that remain elevated and stickier than in goods sectors. It is likely that inflation can fall into the 4- 6% range this year, but the trajectory of getting back below 2% or even 3% could linger into 2024 or beyond. After letting inflation run hot for so long, it seems that the Fed will not be in a hurry to embrace some of their former policies quickly barring a financial crisis or rapid weakening in economic conditions.

The economic forecast in 2023 is much murkier than in recent years. In 2021, when earnings were robust, the economy had recovered from COVID quickly and interest rates were near zero, it was fairly obvious that conditions would soften and interest rates would rise in the future. Now, it remains an open question of when (or if) the U.S. economy goes into recession, and how dramatically the Federal Reserve will reverse course to fight economic weakness, versus finishing its commitment to put the inflation genie back in the bottle.

Equity Tactical Allocations

We remain slightly underweight equities in our portfolios relative to our investment objectives. We did not change our equity position in 2022; valuations in stocks overall improved to counteract technical weakness in prices and deterioration in leading economic trends, both unfavorable to adding exposure.

We continue to favor value-style equities but have increased our emphasis on smaller and mid-sized companies within those sectors. We were pleased to correctly predict that larger companies, particularly in the growth sectors, would be damaged by shrinking liquidity and central bank policy changes. Throughout 2022, we did notice certain stocks and sectors become “safe haven” trades, or places to hide out away from the most challenged parts of the market. For a while, some of the largest stocks were safe havens, until ultimately almost all of them had a deep correction over the course of the year. However, many of the larger stocks in sectors such as health care, consumer staples, and utilities held up very well or even rose in price during 2022. If the economy goes into recession, we see equally high risks in these stocks and prefer smaller companies that do not carry the lofty valuations of the mega-sized companies.

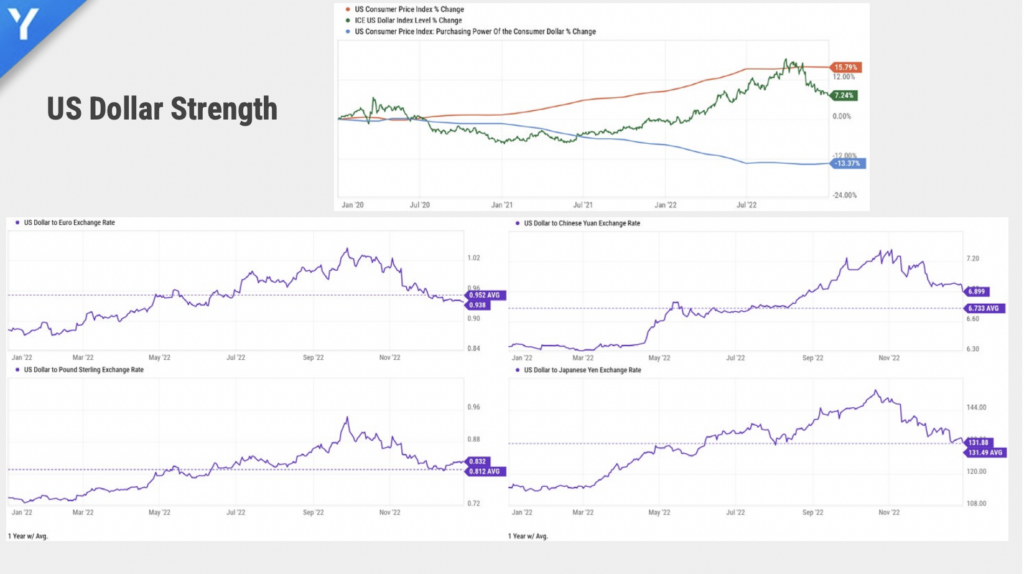

We maintain our current positions in international and emerging markets stocks. International stocks as measured by the MSCI EAFE Index (-14.5%) finally outperformed the S&P 500 following an extended period lagging that index. International stocks inherently have higher exposure to value sectors, which we continue to favor over their growth counterparts. International stocks struggled for much of the year behind the anchor of an extremely strong dollar. The U.S. Dollar Index rose to a 20+ year high in September before falling sharply in the final quarter of the year. As the market saw the Fed’s pace of interest rate hikes slowing, the dollar’s fall provided a tailwind for international stocks, which were already trading at discounted levels relative to the U.S.

Emerging markets stocks as measured by the MSCI EM Index (-20.1%) slightly lagged the S&P in 2022 but rallied late in the year behind the weakening dollar and the economic optimism behind China’s reopening following lockdowns. They also benefited from the risk-on sentiment and hope that a global recession would not be as rapid or severe as feared.

Fixed Income Tactical Allocations

We are also slightly underweight fixed income in our portfolios. During 2022, we reduced our position in inflation-protected securities and added exposure to Treasury and foreign sovereign debt while reducing corporate and high-yield bonds.

Our managers remain slightly underweight duration in portfolios. By the end of 2022, the yield curve had become deeply inverted, with short-term rates offering much higher comparable yields than longer-dated securities. We have increased bond portfolio quality and are cautious on credit with the possibility or likelihood of a recession in 2023.

We remain underweight municipal bonds relative to taxable bonds. Municipal bonds offer historically narrow spreads versus Treasuries, particularly in shorter maturities. For our clients that benefit from tax-exempt bonds, we continue to use other fixed-income sectors to complement their municipal exposure.

We maintain a position in high-yield and emerging market bonds, though we did swap some of our investment for a new allocation to developed international bonds during mid-2022. We saw the historically expensive dollar as an opportunity to add exposure to non-dollar-denominated fixed income. Many central banks in the developed markets are following a similar track to the Fed with interest rate increases and an end to quantitative easing. Even Japan, a proponent of yield curve control for decades, has begun to hint at allowing rates on their bonds to drift higher, which has strengthened their currency versus the dollar.

Alternative Investment Tactical Allocations

We maintained our exposure to alternative investments during 2022. Our strategies, particularly managed futures, provided excellent uncorrelated returns in a historically difficult year for both stocks and bonds. Event-driven managers also turned in positive results and were excellent diversifiers to traditional asset classes.

We are mindful these strategies will likely not continue the pace of outperformance (i.e. 10-30%+) on an annual basis versus stocks and bonds. We are maintaining these positions because we do not think that we have reached the end of the bear market cycle. We expect some periods of heightened volatility in 2023, which may cause us to reevaluate our positioning if the economic cycle or valuations shift more favorably toward stocks.

We continue to consider private investments on a selective basis. Given the valuation reset in public markets during 2022, we expect that many private funds will begin to mark their portfolios lower this year. This may provide an opportunity to add new positions at better valuations or consider secondary funds that are seeking new investors or liquidity, and offer better entry points for that asset class.

Strategy Update

Our equity strategy turned in a strong run of outperformance relative to both U.S. and global benchmarks. Our strategy portfolio was up 12.3% in the fourth quarter of 2022 versus 9.8% for the MSCI ACWI (All Country World Index) and 7.6% for the S&P 500. For the calendar year 2022, it finished down -12.1%, with those benchmarks returning -18.4% and -18.1%.

Our taxable fixed-income strategy also outperformed its benchmark in 2022. The strategy was up 4.56% in the fourth quarter of 2022, compared to 1.87% for the Bloomberg U.S. Aggregate Bond Index. For calendar year 2022, it finished down -11.8% vs. -13.0% for that benchmark.

Our tax-free fixed-income strategy was up 4.4% in the fourth quarter of 22, compared to 3.6% for the Bloomberg 1-15 Year Municipal Index. It finished 2022 down -6.1% vs. -6.0% for that benchmark.

Our liquid alternative fund strategy finished the fourth quarter down -2.3% but still was up 8.8% for 2022. It was led by our largest holding, a managed futures strategy which was up 17.1% for the year.

Final Thoughts

As we turn the calendar to 2023, we look ahead with a mix of optimism and concern. We wrote last year about how our outlook was dominated by challenges, rather than opportunities. We correctly forecast many of the challenges the market faced and attempted to steer portfolios away from the greatest dangers. Now, we see the pendulum moving back toward opportunity, but do not spot many of the classic signals that accompany a market bottom or excellent entry point for adding risk.

Ever since the Fed started aggressive rate hikes last summer, the market has seemed to anticipate the end of their cycle and returning to a world of lower interest rates and easier monetary policy. Even in the first few weeks of January, stocks are off to a strong start, based on the belief in a “soft landing”, that inflation will abate while the Fed will pause and ultimately lower interest rates without the economy suffering much damage.

We see this outcome as a low-probability event. We expect that the effects of 2022’s rate hikes are still being absorbed into the economy. While the bond market may be correct that future rates will be lower and inflation will trend down, it is likely to be due to economic weakness and continued deterioration in earnings trends. The job market has been unusually strong so far in the face of the Fed’s action; however, if job losses do not materialize in a meaningful way, we do not expect the Fed will be keen to lower interest rates much this year. The U.S. economy must prove that it can thrive in a higher-rate environment, something it has not had to do over any sustained period since last century.

Our expectation is that the economy will slow during 2023 and while inflation will continue to drift toward the Fed’s targets, it will not be enough to cause them to reverse course on policy. We see earnings estimates continuing to adjust down because of higher input costs and lower profit margins. The stock market, which had a near-term low back in October, has rallied about 15% from that level and is trading at full valuations even without a recession; if one appears this year, we fully expect large-cap U.S. stocks to retest or go lower than that October level.

During bear markets, typically the bottoming process forms during the middle or late stages of interest rate CUTS. It would be extremely unusual for the stock market to bottom 4+ months before the Fed stopped raising rates. The October low for the S&P 500 would also represent, on many metrics, one of the most expensive valuations for a bear market trough in history.

We see the weight of the evidence indicating the stock market still to be in the middle of a bear market cycle. Perhaps the most similar pattern in recent history was the 2000-2002 bear market, which took about two and a half years to complete from peak to trough. There were several sharp rallies and false starts in that cycle, and w see some similarities to today’s action.

However, we are very optimistic about several asset classes, both in this cycle and the next bull market. We see small and mid-cap value US stocks as offering solid long-term returns; both are trading below historical average valuations. The same can be said of international and emerging market stocks, particularly in value sectors. If the dollar continues to trend lower this year, we could find a scenario where international stocks are positive this year, even if the U.S. market is flat or down. If the US or global economy goes into recession, we think these stocks provide enough margin of safety that is worthwhile to buy at these levels, even if there may be some better entry points ahead.

Last year, we promised that we were adjusting our portfolios to the market of tomorrow, rather than yesterday. While we are not satisfied with losses, we’re pleased we were able to help clients protect more of their capital in a bear market and in many cases, avoid the downside of owning the market index portfolio last year. We correctly forecast that the portfolio of yesterday (large-cap growth U.S. stocks) would probably be one of the most troubled areas to invest in. We remain convicted that a leadership shift is underway and many of the winners of the last decade will likely be out of favor for some time. We still see too many investors and advisors eagerly buying the dip in the stocks of the last cycle; usually by the end of a bear market, investors tend to “throw in the towel” on old favorites, and we have yet to see broad capitulation across markets. There has been progress made in sifting through the most speculative areas, but we expect there is still room to go. We are eagerly looking for signals and opportunities to shift tactics and take advantage when the next bull market arrives.

Thank you for your continued confidence during the past year. As always, please contact any of our investment team members if you want to review your strategy or learn more about our ideas and how they apply to your specific objectives.

Email Signup

"*" indicates required fields