April 21, 2023

2023 First Quarter Investment Update

Bear Market Rally or Bull Market Renaissance?

The first quarter of 2023 showed markets to be resilient following an incredibly challenging and volatile 2022. Both stocks and bonds rallied despite signs of economic slowing, along with fears of bank failures and financial system contagion. Inflation continued to drift lower but well above Federal Reserve targets. Corporate profits slipped but hopes of a Fed pause in interest rate hikes and an end to tightening monetary policy provided optimism to the outlook for the remainder of the year. Most notably, the banking crisis in early March created a new wrinkle in the economic outlook, as investors took sides debating whether a “hard” or “soft” landing was in store.

One of the catalysts for the stock market was a pause in the relentless march higher of interest rates. After peaking to a new cycle high above 5% in early March, the 2 Year Treasury note yield plummeted below 3.8% before recovering to 4.06% by the end of the quarter. The 10 Year Treasury followed a similar trend, rising above 4% briefly before falling back below 3.5% at quarter end. As the bond market began to price in Fed rate cuts in the second half of 2023, the stock market interpreted it as a signal to “risk-on” investments, causing higher valuation and more speculative assets to outperform.

In response to the failures of Silicon Valley and Signature Banks, the Federal Reserve created the $300 billion Bank Term Funding Program (BTFP) to support financial institutions who faced capital drawdowns. This amount, while not directly injected into the economy like many of the former “quantitative easing” bond buying programs, was seen as a new form of monetary stimulus. Gold and crypto assets rallied as investors sensed a new era of money printing may be underway. As of now, the Fed continues to draw down its balance sheet via their established QT program, although BTFP effectively added back about half of the amount drawn down by the Fed since last summer.

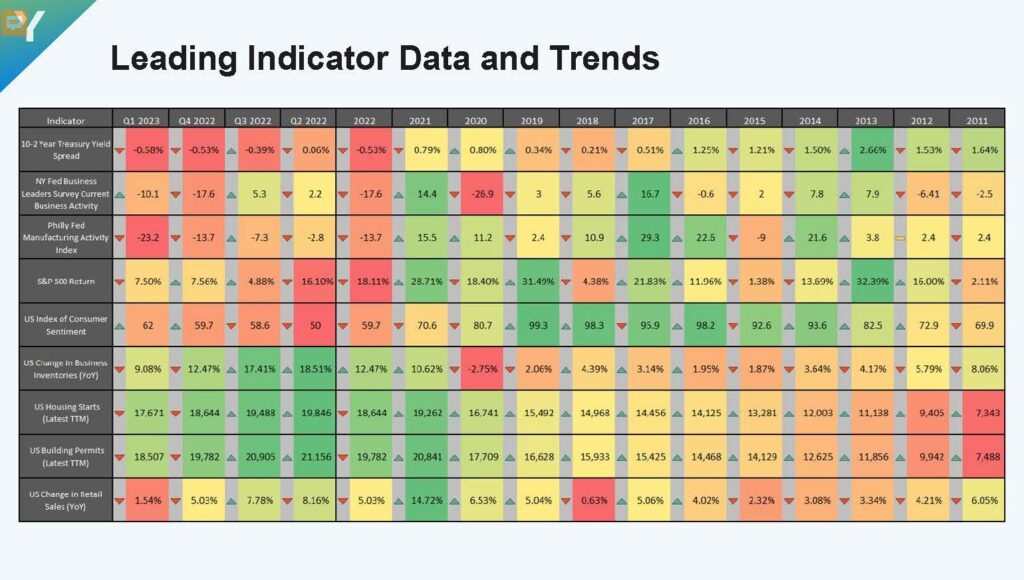

As the quarter ended, there was no obvious new threat or sign of stress that caused investor concern or a shift in Fed sentiment on inflation. The economy continues to show signs of late cycle characteristics. The unemployment rate still sits at 3.5%, though job openings are dwindling and jobless claims have been on a steady uptick in recent weeks. Headline inflation (CPI) fell to 5.0% in March, but notably Core CPI remains at 5.6% due to cooling of food and energy prices but stickiness in shelter and services costs.

The Federal Reserve is expected to raise interest rates once more in May, by 0.25%. After that action, there is a disconnect to be resolved between the market’s expectations and Fed guidance for the rest of the year. Most Fed governors have publicly been supportive of a “higher for longer” interest rate policy, where current rates will remain elevated until it is clear inflation is nearing their 2% target. Meanwhile, market participants see multiple rate cuts by the end of the year. Which side is correct, and for what reason, will likely dictate where markets head for the rest of 2023.

Solid Start to the Year, but Breadth Lacking

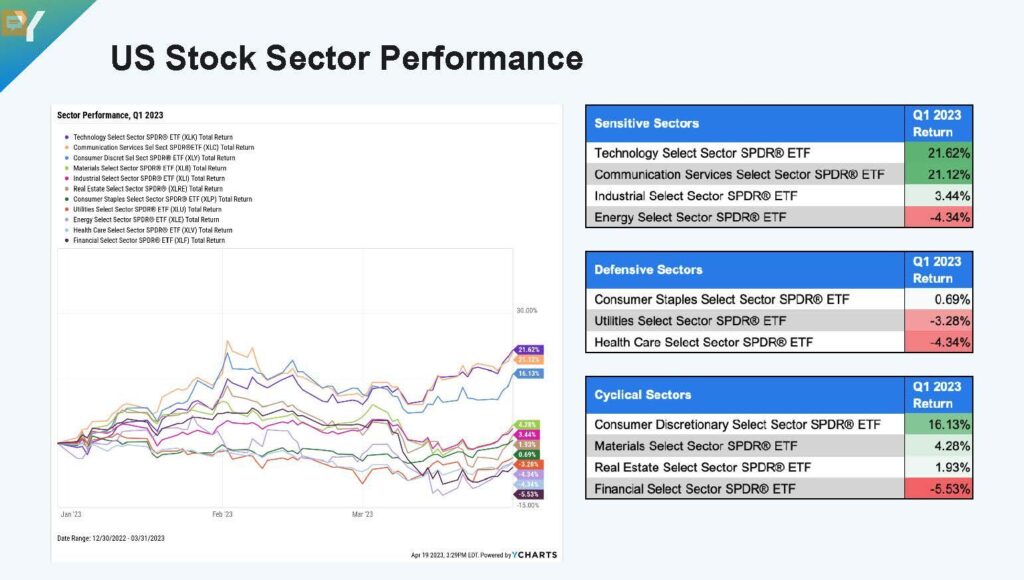

The year began with an almost immediate rally in the stock market, as many of the companies and sectors that most underperformed in 2022 reversed trend. A handful of the largest companies in the S&P 500 delivered outsized results that lifted the index higher while many smaller and mid-sized companies had fairly tepid returns. Two of the standouts included Nvidia (+90%) and Tesla (+68%) while Apple, Microsoft and Amazon all had returns exceeding 20%.

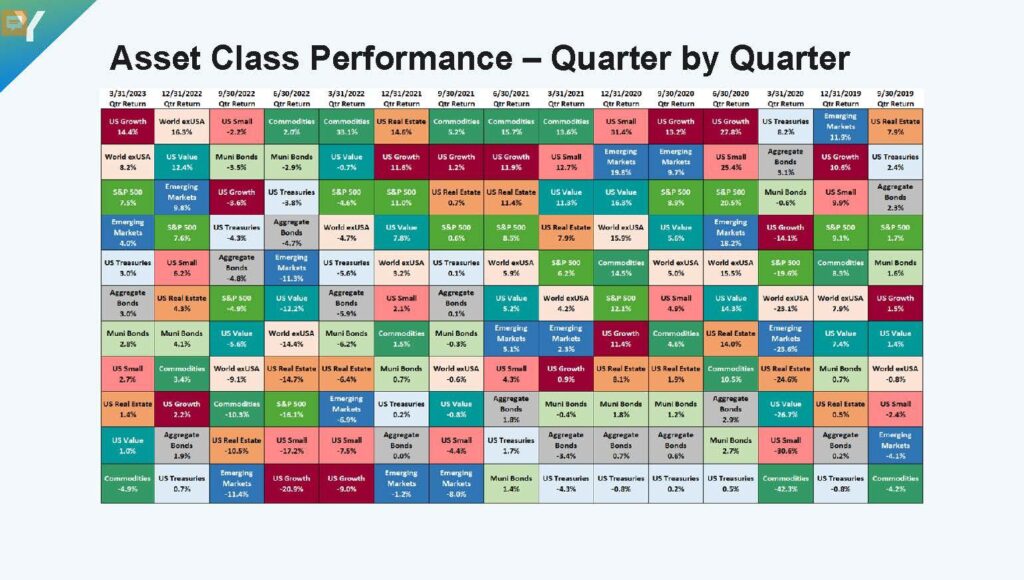

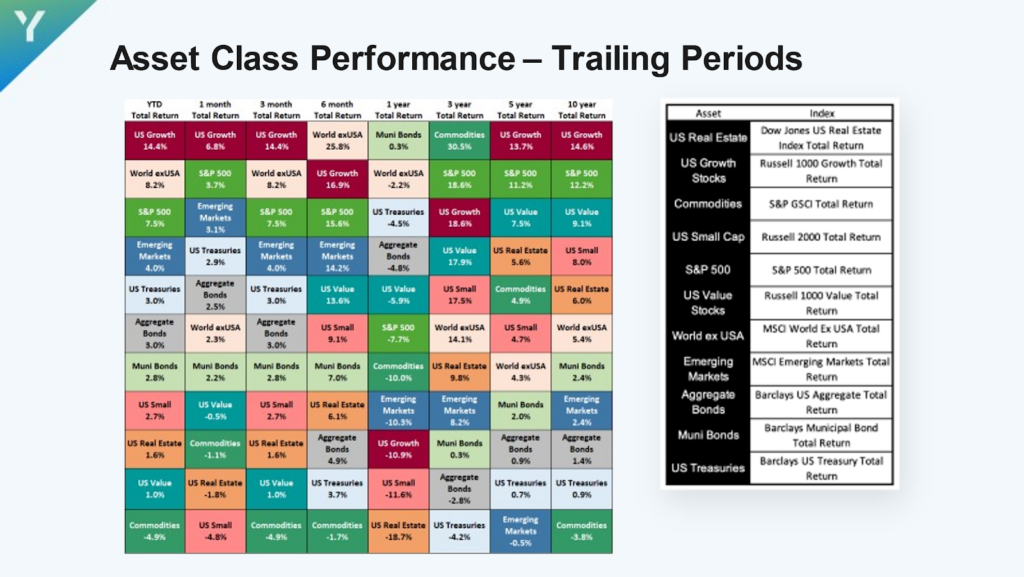

Large cap US stocks (as measured by the Russell 1000 Index) were up 7.5%, while small cap US stocks (Russell 2000) were up only 2.7%.

International stocks (MSCI EAFE) continued their strong performance from the fourth quarter, posting an 8.5% return. Emerging markets (MSCI EM) were up 4.0%.

All sectors of the bond market benefited from the cooling of interest rates, and credit stress eased after the banking crisis. US taxable bonds (Bloomberg US Aggregate Bond Index) were up 3.0% and municipal bonds (Bloomberg Municipal 1-15 Year Index) were up 2.3% in the first quarter. Corporate high yield bonds were up 3.6% while international bonds up 3.1%, benefiting from a weaker dollar and higher interest rates abroad.

There was a wide dispersion in returns between growth and value stocks in the first quarter. After an exceptional run in 2022, the value style lost ground in the first quarter, as the mega-cap stocks in the US dominated. There was over a 14% return gap in performance between large cap growth and value stocks in the quarter (as measured by the Russell 1000) and about 7% between small cap growth and value.

Strategy Update

While our absolute returns were very respectable in the first quarter, relative returns were disappointing for our equity tactics that continue to favor smaller, lower valuation companies. Our equity strategy finished the quarter up 5.4%, or about behind 2% the broad US and global benchmarks.

Our taxable bond strategy had a better showing during the quarter, up 3.6% and outperforming the Bloomberg US Aggregate Index. Our municipal bond focused strategy also had a strong start to the year, up 2.8%. Our satellite positions in inflation protected securities (TIPS), high yield bonds and emerging market debt all were additive to returns.

Our alternative investments did not perform as well in a period of trend reversal, lower volatility and risk-on sentiment. Our core alternative strategies ranged from slightly positive (event driven funds) to down about 4% (managed futures) and were the weakest performing allocation in portfolios after being the strongest throughout much of 2022.

Outlook Update

After such a strong start across markets, it does lead us to revisit the thesis guiding our tactical outlook and positioning. This bear market cycle is notable for having many patterns that defy historical parallels. Market observers have been able to identify examples that often start with “when X happens, Y always occurs, or Z never does” and yet the market has often confounded those comparisons. We expect this one will continue to surprise investors throughout the remainder of the year.

We remain convicted that the market is in a bear cycle that began in late 2021/early 2022 and not in a new bull market cycle or uptrend. There are several data markers we see that support this belief.

First, the breadth of the market rally is not indicative of a new cycle. The leadership of the market is concentrated in a few stocks, while many others have languished and are not far above the bear market low last October. Usually in new bull markets, there is broad participation across all types of companies. The market behavior is more indicative of a fear-based reaction where investors are “hiding” in the largest names expecting a slowdown in growth and/or new Federal Reserve monetary support to justify higher than normal valuations seen in 2021.

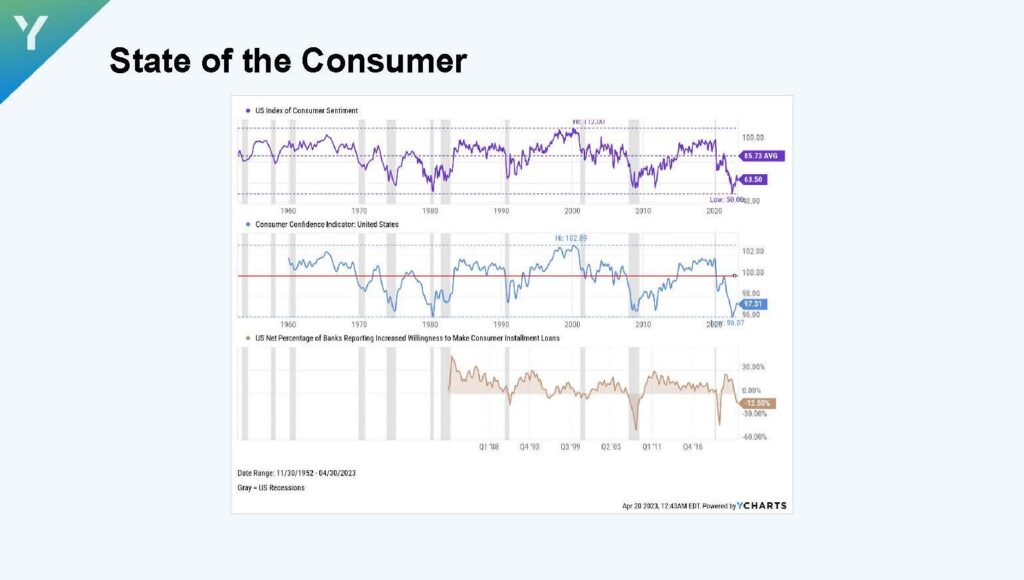

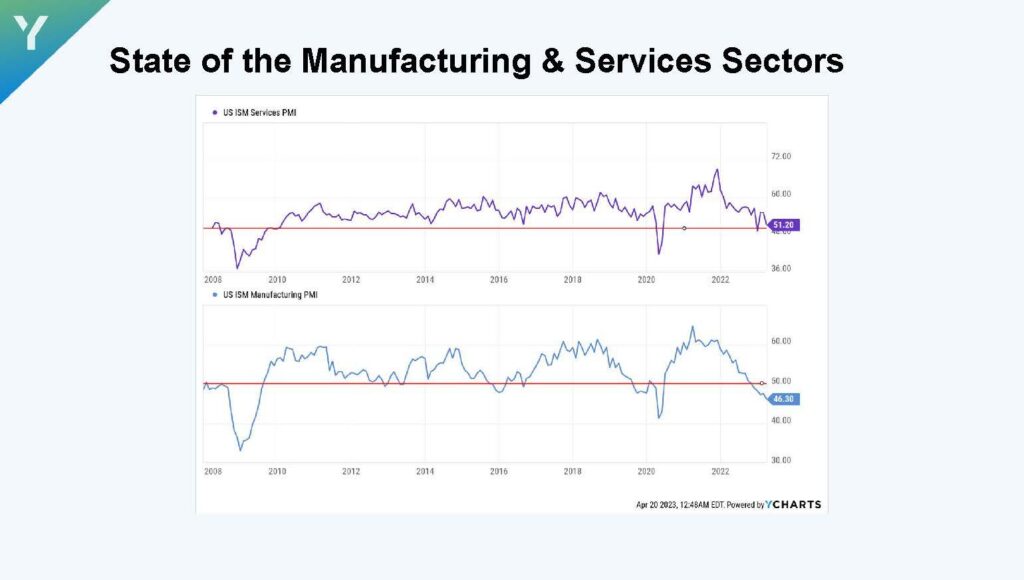

Second, economic trends are not supportive of a surge in activity and spending that would align with continued growth and momentum in 2023. With the Fed’s collective 5% rate increase taking hold, there has been a slow but steady deterioration in both the job market and industrial output. Consumer credit card balances are nearing $1 trillion and almost all Americans hold a mortgage with a lower rate than what is available today. The past two months have seen a decline in retail sales versus expectations, and we see consumers being more cautious with discretionary spending with continued high inflation. At the beginning of a bull market, you expect to see “new money” in motion as workers rejoin the job market and contribute to spending and investment. Currently, we see the opposite.

Third, the valuation and attractiveness of the US market does not support a sustained rise with the relative opportunity of cash and money markets. The S&P 500’s equity risk premium, which is measured as the spread between the earnings yield of the market vs. Treasury Bills, is at its lowest level in over 20 years. Based on the S&P’s forward price to earnings ratio of just over 18, investors are accepting about 5.5% in earnings yield on stocks. Usually, investors demand a premium return of 3-4% over cash, and often higher amounts in periods of economic uncertainty. Today, that return is about 1% with Treasury money market yields sitting around 4.5% (and expected to go up with a rate increase in May).

Our expected outcome is that the economy will enter a recession later this year, as the effects of monetary policy continue to impact businesses and consumers. There is a considerable lag time associated with any interest rate change, and we are now just past the one-year anniversary of the Federal Reserve beginning their campaign. We expect peak effects will not be felt until later this year, and although difficult to predict, there will likely be other financial and credit stresses like those seen with the failed banks in March.

Earnings estimates for U.S. stocks in 2023 have been in a steady decline since last year, and the analyst consensus for the S&P 500 expects a strong uptick in growth in the fourth quarter. We do not see a catalyst for growth to reaccelerate given the conditions discussed and expect estimates will continue to be revised lower, putting pressure on valuations.

We continue to favor value-oriented strategies and are reducing some of our exposure to market cap weighted index funds that have a higher allocation to larger growth stocks. We do not see those companies as havens in this environment, as their valuations are effectively pricing in little to no recessionary impact. With the damage caused from the banking crisis, small cap stocks are trading at relative lows last seen in late 2020 before their strong run of outperformance. We see a reversion in performance over the next year occurring through a combination of factors. If we enter a recession, earnings revisions and valuation contraction are likely to be more acute in larger growth stocks. Also, if the market begins to look ahead into 2024 and an economic recovery, small cap stocks should lead due to their cyclical nature and room for valuation expansion.

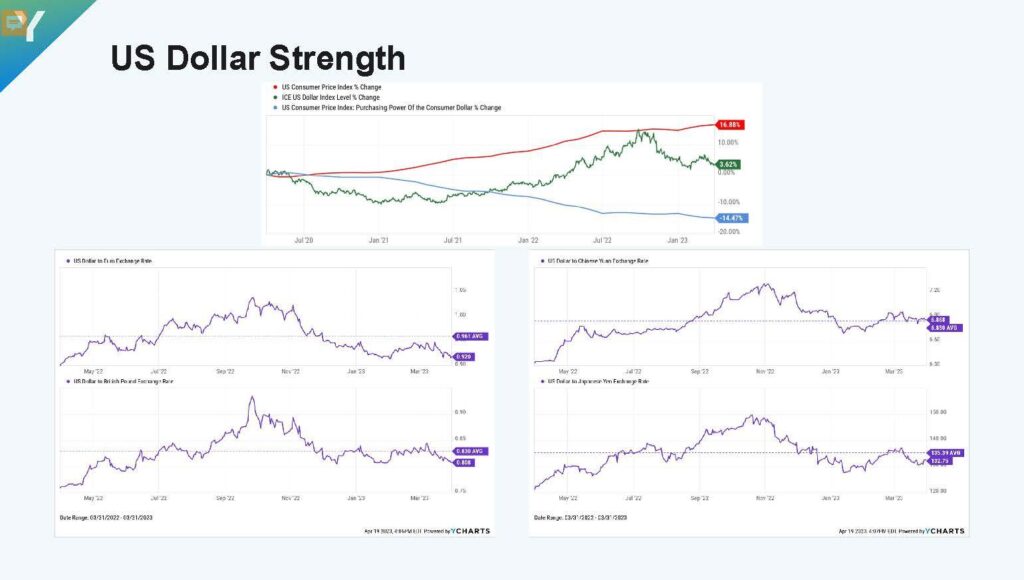

We are maintaining our allocation to international stocks; as expected in some of our recent commentary, the dollar has weakened as the U.S. economy shows signs of slowing and the Federal Reserve nears the expected end of their rate hiking cycle. Many other global central banks are still in catch up mode relative to the U.S. with rate increases and quantitative tightening of their balance sheets and money supply. Europe’s economy has shown better than feared resilience from the effects of higher energy prices and the Ukraine-Russia conflict. Japan’s new central bank governor has signaled they may start to unwind longstanding yield curve control, meaning their interest rates may start to rise relative to other countries and strengthen the yen as a currency.

We continue to overweight emerging markets in our equity portfolios. They should also benefit from the weaker dollar, as well as an inflationary environment that favors materials and commodities-oriented investments more prevalent in these countries. Most emerging markets continue to trade at a significant valuation discount to the U.S. While this has been the case for some time, we expect that the acceleration caused by China’s economic reopening should help boost the outlook for EM and cause investors to gravitate toward their secular growth trends with stagnant growth in the U.S. and some developed markets.

In our bond portfolios, we are reducing high yield exposure and increasing our allocation to high quality fixed income. We see the potential for corporate credit deterioration in a recessionary environment. We believe investors are receiving a very fair return in higher rated bonds as we expect to enter a more challenging period later this year.

We are maintaining our current alternative investment allocation. As of this writing, volatility is at its lowest levels since the bear market began. We expect managed futures will provide protection against unpredictable shocks throughout the rest of the year, as well as inflation if it remains stubbornly high. Seasonally, the market enters a more challenging period after April, and with the current relative complacency, we see this defensive allocation as key to managing through risks and uncertainties.

Bear markets are, by nature, tricky to navigate because they occur less frequently than bull markets. Stocks tend to rise about 2/3 of the time, and it is a losing proposition to bet against them over the long run. However, how an investor performs during a bear market can be critical to their long-term results because deeper losses require greater gains in a recovery. For our clients in 2022, we avoided downside through our positioning in value stocks and alternative investments. We look forward to tactically getting bullish on the stock market in general, but do not think now is that time.

During the 2000-2002 bear market, there were five instances where the technology heavy NASDAQ Composite index entered a “faux bull”, rising 20% from the prior low only to break to a new low again before the cycle ended. There are constantly debates during bear markets about whether “the low is in”. Rather than obsess about that timing, we advise taking advantage of available opportunities, of which there are many more than a year ago. Cash is currently yielding about 4.5% annually, and that level is unlikely to drop off much this year. Bonds are offering similar yields with additional protection if an economic shock happens and interest rate expectations drift lower. Small cap value and international stocks trade at levels that typically deliver compelling long-term returns and have arguably discounted recessionary or stagnant growth / higher inflation scenarios in prices. There are solid opportunities in the current market, but we encourage investors not to focus on hype and headlines, avoid chasing hot stocks in 2023 or indexes like the S&P 500 and NASDAQ, two of the less attractive options we see now.

Thank you for your confidence in our stewardship of your and your family’s wealth. Please contact any of our advisors if you would like to discuss how these ideas may apply to your investment strategy and financial plan.

Email Signup

"*" indicates required fields

Chattanooga

Union Square Suite 600

Chattanooga, TN 37402

Nashville

3100 West End Ave Suite 860

Nashville, TN 37203

Atlanta

3290 Northside Parkway NW, Suite 850

Atlanta, GA 30327