February 04, 2026

Southeastern Trust Investment Memo

Next Play

In the sporting world, it is common to observe coaches at the postgame press conference quickly recap the events of the game just completed, while pivoting to a discussion of the next game, the next practice, or even simply the next play. Their explanation is usually that once the game is over, there is nothing more that can be done to undo the result; the outcome is final and the record is permanent. It may even be counterproductive to take too much confidence from a win because in the next game, the score always begins zero to zero again. The best tactic is to focus on the controllables of how you will prepare for and execute the next play.

In investing, it is instructive to look back at the events of the past as a guidepost for the future. As your advisor, we believe it is important to provide an explanation of what happened in markets and the economy, and how we reacted to those conditions.

That said, the concept of Next Play is useful in investing. Yesterday’s performance may provide some clues about what tomorrow will bring, but in some ways, it is a completely new game. As an investor, you must be conditioned to understand lessons you can take from the past. However, you often must prepare for a new “scouting report” of economic, political and market events that may challenge the strengths of your portfolio and investment philosophy, or expose weaknesses. Below are some highlights of this memo that summarize recent trends and our outlook.

Executive Summary

- Foreign stocks and bonds made a strong comeback in 2025, supported by a weaker US dollar and improving relative earnings trends in international markets. We have favored these stocks in client portfolios throughout the past year and continue to recommend a global balance of assets.

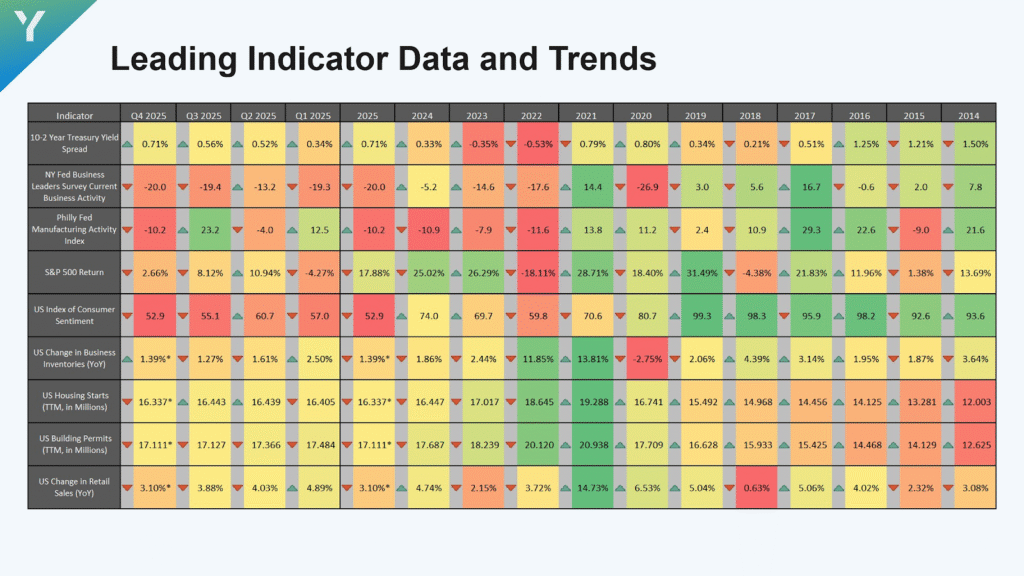

- The U.S. economy is a mixed picture. It is being supported by high levels of government deficit spending, a Federal Reserve inclined to cut interest rates, and the momentum of technology spending concentrated in artificial intelligence. However, some segments of the economy remain or are increasingly stagnant; housing, manufacturing and retail have all been challenged, and there is evidence that middle- and lower-class consumers are constrained by inflation and are not benefiting comparably from rising asset prices.

- The U.S. stock market also shows conflicting signals. There has been improved breadth and performance across multiple market capitalizations and sectors in recent months. Bull markets typically end with a narrowing, rather than a broadening of leadership. However, large cap growth stocks are trading at some of the most expensive valuations in history. About one third of the S&P 500 companies trade at over 10 times their current sales. There is no historical precedent for stocks this expensive to deliver future returns near historical averages; returns have been below average or even near zero over the subsequent 10 years. Retail ownership of stocks and margin debt levels are also near historical highs compared to previous cycles and return patterns.

- Fixed income markets offer reasonable to good values compared to historically expensive segments of the stock market. Given narrow credit spreads and continued large fiscal deficits globally, focus on high quality bonds, allocate to inflation protected securities and diversify currency risk with international fixed income.

- There is a push and pull to the stock market which causes us to maintain our current neutral stance until the evidence changes. Index valuations and leverage are extremely unattractive using history as a guide. However, the fiscal and monetary support for the economy may continue to extend the market cycle for a few more quarters or even a year. Technical trends and momentum across sectors are positive. With valuations this expensive, it is possible that conditions and sentiment could change rapidly and even good results may not be “good enough” to justify prices. We are monitoring the credit markets and breadth of the stock market’s leadership for clues about shifting to a defensive stance.

Calling an Audible: “American Exceptionalism” Becomes “Sell America”

The financial media is known for coining easy to remember phrases to explain the investment theme or popular trade of the moment. Most are familiar with the “Magnificent Seven”, commonly used to represent the seven largest companies in the Standard & Poor’s (S&P) 500 Index. The phrase no doubt became popular in the investment landscape due to the outperformance of those stocks versus all other companies in the U.S. market.

Another theme which cropped up in recent years has been the term “American Exceptionalism”, often used to describe the phenomenon of U.S. stocks outperforming the collective return of the rest of the world. There have been some valid reasons for the outperformance; US companies have grown earnings at a faster pace than other countries since the global financial crisis of 2008, while the US dollar has generally been supportive as a currency.

But like all investment trends, there is usually excess both at the peak and trough of cycles. Entering 2025, the US stock market traded at one of the widest valuation premiums in history compared to the rest of the world – almost double the valuation of the developed international markets and more than double that of emerging markets. Even if the US continued to maintain its prior growth and earnings momentum, it was highly likely that premium was already priced into those stocks, or excessive despite these conditions.

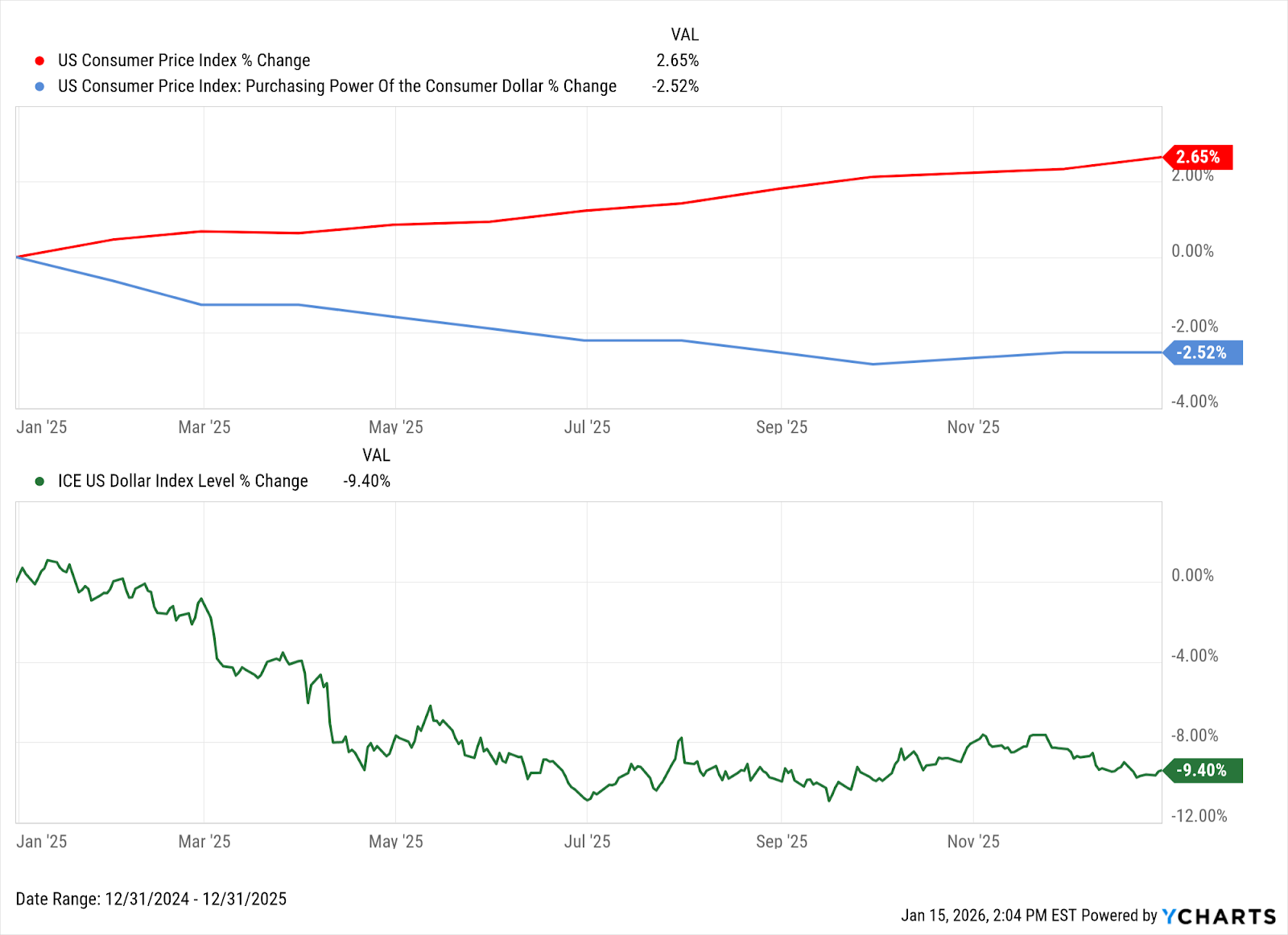

That valuation phenomenon is one in which we will revisit in other aspects of last year’s and today’s market. In 2025, both before and during the height of the tariff fears, it was apparent that a shift was underway in the market’s view of both US and international stocks, but also the dollar versus other currencies. The dollar index fell 9.4% in 2025, its worst year since 2017. That factor, combined with improving earnings outlook in foreign markets and a not bad as feared outcome from tariff and trade negotiations, allowed the MSCI EAFE (developed) and EM (emerging) indexes to climb over 30% in 2025, easily besting the S&P 500 return of 17.9%.

By the end of 2025 and into early 2026, the “American Exceptionalism” meme had morphed into a new phrase: “Sell America”, reflecting the weakening dollar combined with concern about the economic outlook due to trade and a concentrated market in technology and artificial intelligence companies.

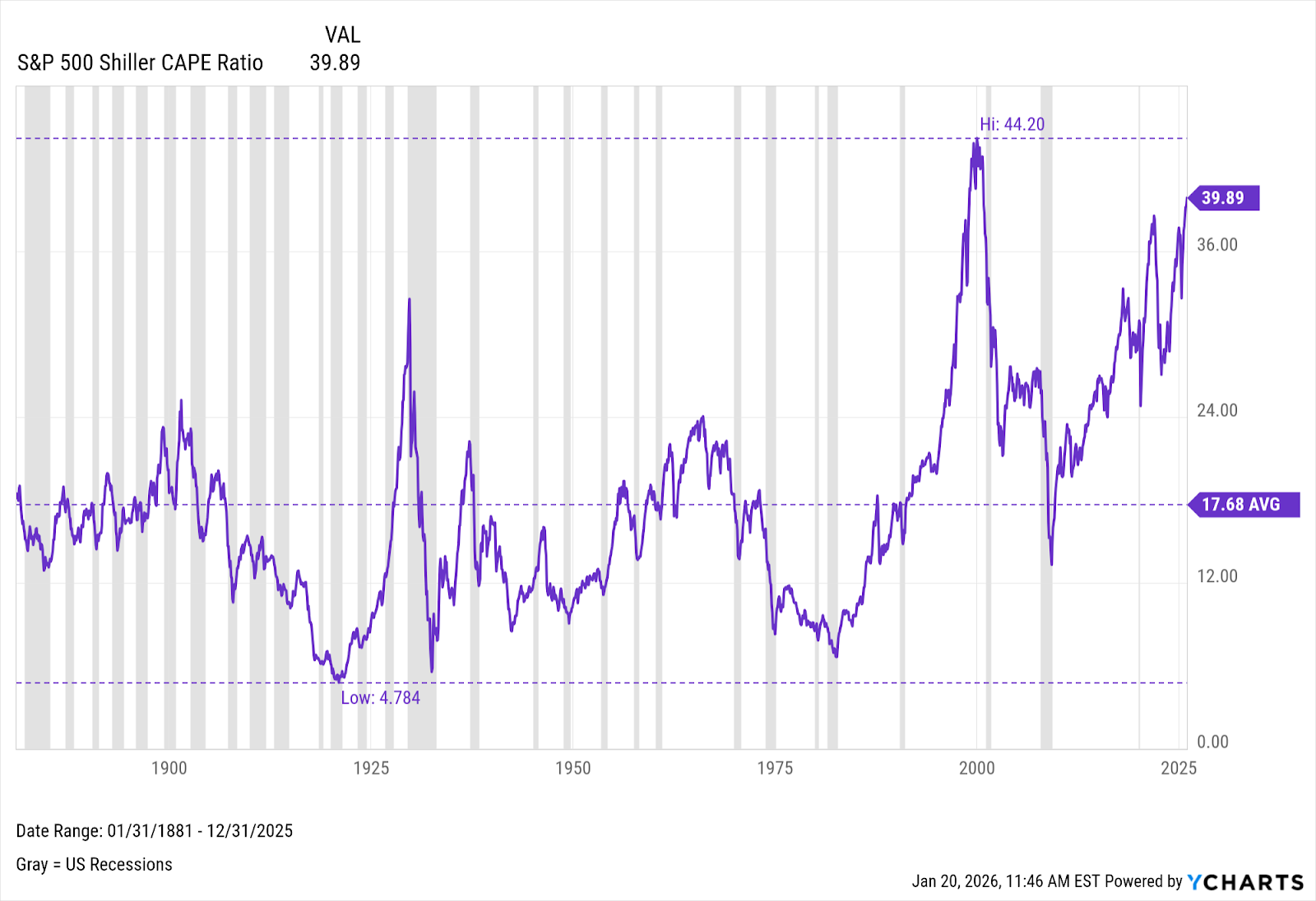

Which theme will be dominant in 2026? We have been advising clients to maintain globally diversified portfolios and have a representative allocation to companies outside the US. Even though international stocks outperformed in 2025, there is still a similar valuation gap compared to one year ago. While it may be unlikely that the dollar as a currency will drop as much as last year, the growth prospects of US stocks will be highly dependent on the performance of the Magnificent Seven, which in turn have become beholden to AI related sales growth and monetization. As mentioned earlier, even if earnings guidance for these companies is met, valuations and expectations are so high, it may be difficult to maintain stock price momentum. There are numerous valuation measures which demonstrate US large companies are expensive; one of the most famous is the Shiller Cyclically Adjusted PE (CAPE) ratio, which is currently at about 40 times trailing normalized 10-year earnings. This valuation level was only reached for a few months during the technology stock bubble of 1999 and 2000. While there are differences between today’s economy and top companies versus that era, some of which may support higher valuations, it is also true that the US is now running much larger fiscal deficits. This level of government spending supports today’s companies’ profit margins in ways that are unique to this time, but also likely temporary and unsustainable.

The Home Team (US) Outlook

While the US stock market (as measured by the S&P 500) powered to its third consecutive double-digit annual return, the economy continues to be a muddled picture. It has led to another contemporary phrase to explain its condition: “K-shaped”. The “K” is the split between the upper income consumers that generally own stocks in their personal and retirement accounts, and have seen their balance sheets grow via the stock market or appreciation of real assets. Lower income consumers typically have fewer or no investments or savings on their balance sheet, and have been more susceptible to the effects of inflation and wage pressures. Despite high levels of government spending (the U.S. continues to run about a 6% annual fiscal deficit; the trend level was closer to 3% before 2020), this has not supported broad based spending growth across all sectors of the economy. Business and consumer activity and sentiment have been muted and display a significant disconnect with the stock market, which by itself might indicate a strong economy and robust levels of confidence. The unemployment rate has drifted up from 3.4% to 4.6%, but there has not been an acceleration in jobless claims consistent with an impending recession. GDP growth is expected to be around 3% for 2025, of which about a quarter is expected to be a result of AI related capital expenditures. The economy was also boosted by trade momentum, as a weaker dollar helped exports. Inflation has remained sticky around the 3% level, which limits enthusiasm for interest rate cuts and should keep investors demanding premium returns and lower valuations.

Last year, we were concerned about the narrowness of the US market leadership. While the top 10 stocks still represent a very concentrated percentage of the overall market (almost 40% of the S&P 500), the breadth of the market began to improve late last year as the Federal Reserve cut interest rates and signaled an openness to continue reducing them in 2026. Small and mid-cap stocks closed the performance gap in the second half of 2025 and got off to an outstanding start in January. We favor small and mid-cap companies due to both valuation and economic conditions being favorable in an environment of steady or lower interest rates.

Fixed Income: A Throwback Player

The bond market has probably been somewhat ignored in recent years as investors and the financial press fixate on widely held companies, mergers, IPO’s and the above average returns of the stock market. However, there are several reasons to pay closer attention to bonds in 2026. After over a decade cycle where interest rates were historically low, followed by three years (2023-2025) where stock returns raced past bonds, there is a reasonable chance that fixed income may have its day and offer attractive results and diversification benefits.

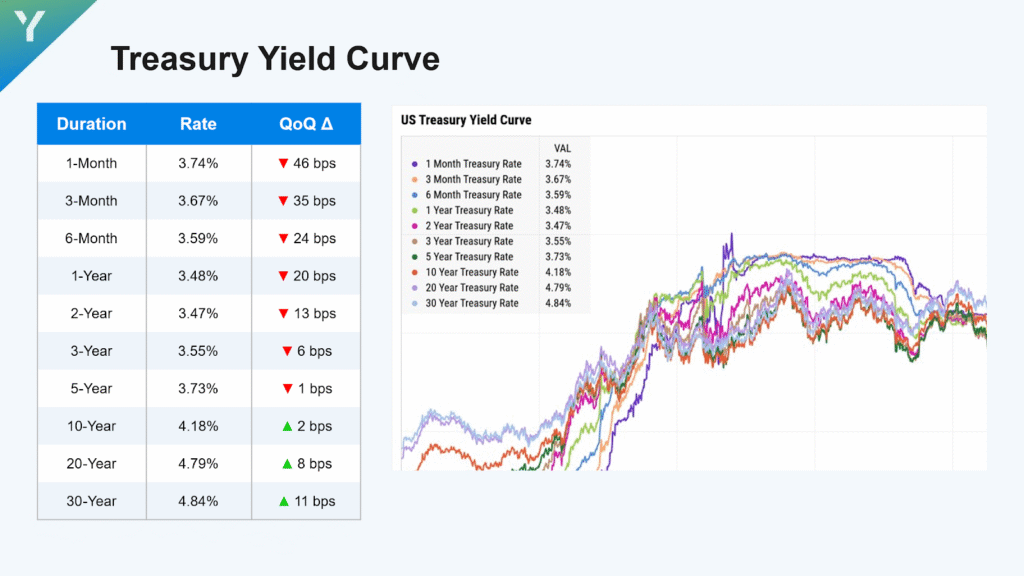

The Federal Reserve cut interest rates three times in 2025, but in doing so, the yield curve steepened, meaning longer duration bond investors are receiving more of a premium return for locking in yields. The improvement in the term premium should entice investors to consider bonds versus cash. Likewise, bond investors can benefit from appreciation in their principal value if rates fall. This could be seen last year in the Bloomberg Aggregate Bond Index, which clocked a solid 7.3% total return in 2025, a mix of income and appreciation. Beyond the index, there were specific opportunities that enhanced those returns. Both international local sovereign debt and high yield corporate bonds offered enhanced income and/or appreciation via strengthening foreign currencies.

The municipal bond market also turned in a respectable year in 2025, although its high yield market did not offer premium returns as with the corporate side. We continue to see good values in municipals, particularly for clients and trusts in higher tax brackets.

Political and Economic Scouting Report

As of this writing, there are many pending events in 2026 that may impact the economy and markets this year. The nominee for the next Federal Reserve Chairman, Kevin Warsh, brings uncertainty about his vision for interest rate policy and the Fed’s balance sheet. The Supreme Court decision on the President’s tariff powers could shift the market’s outlook on their future implementation and the US government’s fiscal situation since many of the One Big Beautiful Bill (OBBB)’s tax cuts and stimulus are currently offset by tariff revenue. The period before midterm elections has often been some of the most volatile in market history. Since the Republican Party controls both Congress and the White House, they are incented to throw the “kitchen sink” at the economy in the form of stimulus this year to sustain momentum through the election. This has sometimes been referred to as the “run it hot” economic playbook, which may lead to continued deficits and above trend inflation.

Current Playbook

*We see the market through the lens of a late-stage economic cycle that has been extended by large fiscal deficits and enthusiasm about technology and productivity gain potential from artificial intelligence. Stock valuations at the index level are some of the most expensive in history. However, we do not invest solely on valuation – to do so would be to miss many excellent returns in the stock market since the Great Recession. But we are mindful that upside is limited and long-term returns will likely be mediocre if you simply invest simply in index funds (especially US large cap).

*Since valuations are generally unattractive, what are some reasons to remain invested or in risk assets? The bond market and credit spreads (premiums) for corporate debt have generally been well behaved. The Federal Reserve is unlikely to pivot to a tightening stance of monetary policy (meaning higher short-term interest rates). The breadth and technical momentum of the market have been solid or even strong in some sectors. If any of these factors begin to deteriorate, it will increase evidence to get more defensively positioned, either reducing stocks or adding diversifiers in a portfolio.

*The extreme volatility in metals commodities and crypto assets is likely a sign of enhanced leverage in markets. Even though the stock market has not shown similar volatility, the elevated levels of margin debt, use of leveraged exchange traded funds and outperformance of low-quality unprofitable stocks late last year signal that it could rear its head with little warning. We recommend using periods of higher volatility as a signal to put new cash to work; with stocks, focus on companies with reasonable valuations and quality fundamentals. Historically, the best time to invest in lower quality assets is at the beginning of an economic cycle, not the end.

*We maintain our outlook on fixed income. Continue to focus bond exposure on high quality U.S. taxable and municipal issues, but hold satellite exposure to local currency sovereign debt and inflation protected securities. Bond yields have been range-bound for some time. We would become constructive adding to fixed income allocations and increasing duration when intermediate-term Treasury yields approach 4.5% and long-term Treasuries are at or above 5%.

*Alternative investments that are diversifiers are likely to add portfolio benefits following strong returns from stocks and bonds last year. Managed futures funds tend to perform well in heightened inflationary environments and periods of high volatility. Both scenarios could play out in 2026.

Investment Outlook

There is a saying in the investment industry that price drives narrative. Whether stocks are up or down, there is always a news article or commentator ready to explain the day’s action with some tidy story or explanation. In March 2009, at the depths of the Great Recession bear market, certainly no one in the media was discussing the potential or could have predicted the 17 years of exceptional returns in the US stock market that were ahead if you invested near the lows. Reasonable or cheap valuations were ignored because there were little earnings (or losses) in many industries. With the benefit of hindsight, it was easy to see that the market was applying very modest valuations or even fire sale prices to depressed levels of earnings and economic output. The worst-case scenarios did not play out, and even “less bad” news was enough to push stocks significantly higher.

Today, with social media, broader coverage of the markets, and instant reactions and analysis on your mobile device, you do not have to look far to find commentators and analysts tripping over themselves to support a bullish thesis. It could be based on any number of themes, technologies or visions. When you block out the noise and focus on price, it is uncanny how the market eventually finds its natural level and the simplest explanation is often the best one. There are likely numerous stocks and sectors at current prices that are applying current levels of growth and extrapolating that same level years into the future. Investors that were pessimistic or despondent that March in 2009 could not have foreseen the S&P 500 going up 25% per year by March 2014. Today, the stock market probably sits in nearly the inverse position. Indexes are priced as if no outcome could dent future growth projections. There are seldom, if any, Wall Street strategists today forecasting stock losses, even though the S&P 500 had a negative return for ten years from 1999-2009 starting at similar valuations as today.

We believe one approach that sets Southeastern Trust apart as a wealth advisor is our focus on the next play and avoiding distractions from the narrative of the last one. It is easy to get comfortable with the winning tactics of yesterday and assume they will lead to a victory tomorrow. It is difficult as an investor, even among professionals, to embrace new strategies and game plans for a distinctive set of conditions. There are good investment opportunities today…but history would lead us to believe fewer ones than at the end of the last bear market in October 2022, and certainly many less than in March 2009.

As winning choices narrow, we commit to being selective in deploying your wealth. We resolve to identify investments that offer the proper balance of risk and return. Finally, we intend to focus on tactics that lead to the outcomes you expect for your investment policy and wealth planning goals.

Next play!

Email Signup

"*" indicates required fields