October 26, 2022

2022 Third Quarter Investment Update

Bear Tracks Abound

Investors rode the roller coaster this summer following the stock market selloff in June. A sharp rally in July and early August was followed by an equally violent reversal in the final weeks of the quarter, leading to a new low for the S&P 500 Index on the final day of September.

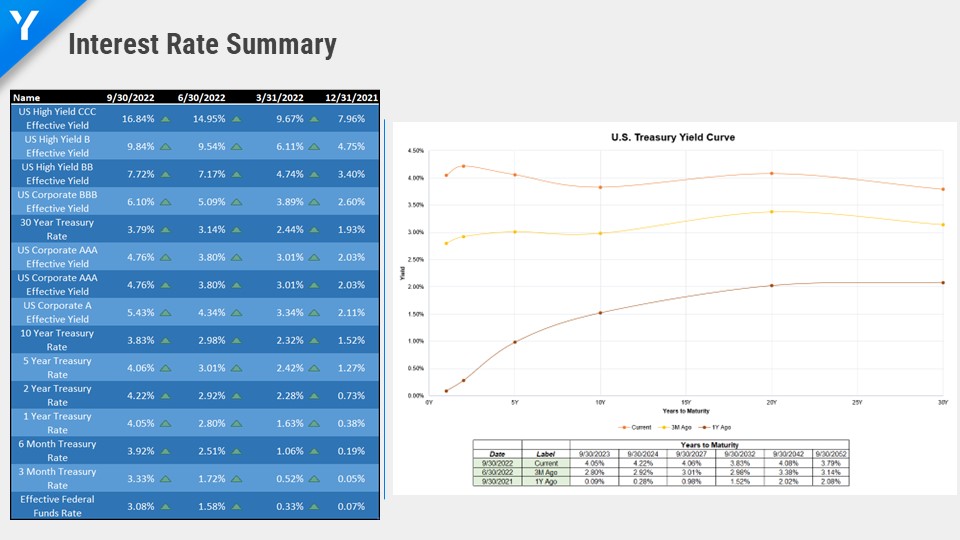

Adding to investor frustration, bond yields continued to march higher as the Federal Reserve affirmed its commitment to fighting inflation. Typically a safe haven in periods of stock market volatility, the bond market has had its own share of turmoil this year. 10 Year Treasury yields rose from 2.98% to 3.83% during the quarter. The now closely watched 2 Year Treasury yield, an indicator of the Federal Reserve’s predicted rate path, increased by 1.3% and ended the quarter at 4.22%.

It was not all bad news, but in an environment where the Fed showed few signs of slowing its aggressive rate hikes, good news effectively became bad news. The economy continued to show signs of resilience, particularly in the labor force. The unemployment rate finished the quarter at 3.5% and jobless claims, while ticking up slightly, have not offered much evidence that higher rates were immediately stalling economic momentum. Corporate earnings have remained generally steady, despite the looming effects of higher funding costs and lower margins.

The primary buzzword of the economy and markets continues to be inflation. The stock market’s rise and fall this quarter can largely be attributed to an inverse relationship with inflation. Hope of a rapid descent in inflation fueled the bear market rally in July; the reality of persistently high inflation prints unwound those gains in August and September.

What Goes Up Must Come Down

The third quarter began with a dramatic rally in the stock market, primarily driven by the hope there was an end in sight to inflation and the Federal Reserve’s path to fighting it. From the June lows to August 15, the S&P 500 Index rallied 17%. On August 26, at the Fed’s Jackson Hole retreat, Chairman Jerome Powell’s speech effectively snuffed out much of that sentiment with a commitment to continued rate hikes and warnings about economic “pain” that would likely result. By September 30, the S&P had fallen 16% from the summer rally peak and ended the quarter down almost 5%.

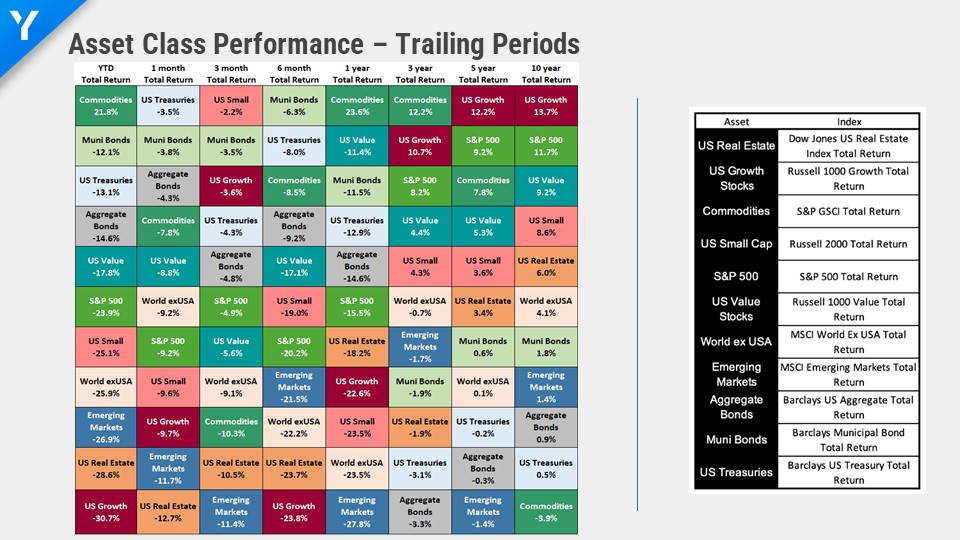

Large cap US stocks (as measured by the Russell 1000 Index) were down 4.6%, small cap US stocks (Russell 2000) were down 2.2%, international stocks (MSCI EAFE) were down 9.4% and emerging markets (MSCI EM) were down 11.6%.

Unlike the first half of the year, leadership in the market briefly shifted back to growth stocks. Hopes of lower interest rates and inflation aided these stocks in catching a bid. Many of these companies were also the most beaten down in the first half of 2022, and as often happens in bear markets, short covering and risk reversals happen in dramatic fashion. Among large caps, growth outperformed value by about 2%; in mid caps (S&P 400), the margin was over 3%, and in small caps, over 4%.

Among fixed income, US taxable bonds (Bloomberg US Aggregate Bond Index) were down 4.8% and municipal bonds (Bloomberg Municipal Bond Index) were down 3.5%. High yield bonds were down less than 1% (a beneficiary of the risk-on sentiment during the quarter), while international bonds were down 10-12%, driven lower by the persistently strong dollar and currency market volatility in the United Kingdom and Japan.

Alternatives Keep Answering the Bell

In stock and bond markets that continued to grind lower, our core alternative investment strategies maintained their record of outperforming. Our managed futures position ended the quarter up 5.7%; while the sector gave back some ground during the July bear market rally, it recovered and hit new highs for 2022 as financial conditions tightened and the stock market reversed course. Our merger and event driven strategies were slightly positive for the quarter, with returns ranging between 0.4 to 1.5%. Over the last decade, it has been a particularly difficult period for many alternatives, especially compared to stocks. However, 2022 has ushered in the first extended period since the Great Recession that central banks have not intervened in markets via quantitative easing (money printing) and low interest rates. As financial conditions normalize and investment fundamentals become more critical, alternative managers should return to form and offer more competitive returns.

Strategy Update

In isolation, the third quarter was the story of a bear market in transition. Often, some of the sharpest rallies come in the midst of bear markets; as the rally builds, investors may start to question whether they missed the bottom of the cycle or the worst is over. We have remained steadfast in our belief that the bear market is not over.

By remaining tilted toward lower valuation stocks and more profitable companies, our equity returns have been very competitive this year against US & global benchmarks. We were validated by the end of the quarter as the stock rally fizzled and the market gravitated back toward these types of companies. During the quarter, our equity returns tracked slightly behind the MSCI All Country World Index but remain almost 4% ahead in 2022.

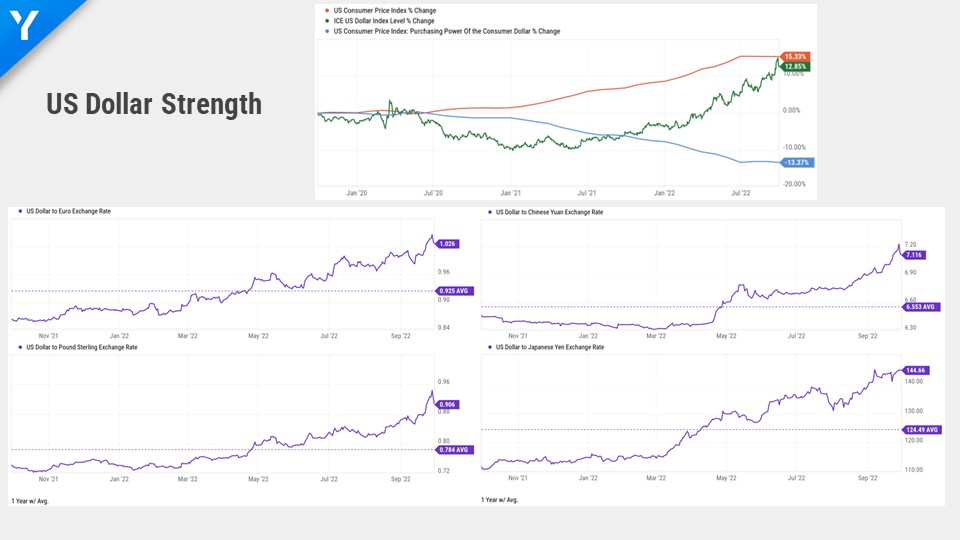

Our taxable bond strategy also trailed the Bloomberg Aggregate Index benchmark by about 0.2% for the quarter and is now behind about 1% year-to-date. Our municipal bond focused strategy also trailed its benchmark last quarter and is behind by a similar margin this year. The primary culprit for our underperformance has been the incredible rally of the U.S. dollar and its effects on our foreign bond allocations. The dollar stands at multi-decade highs against several developed market currencies.

Outlook Update

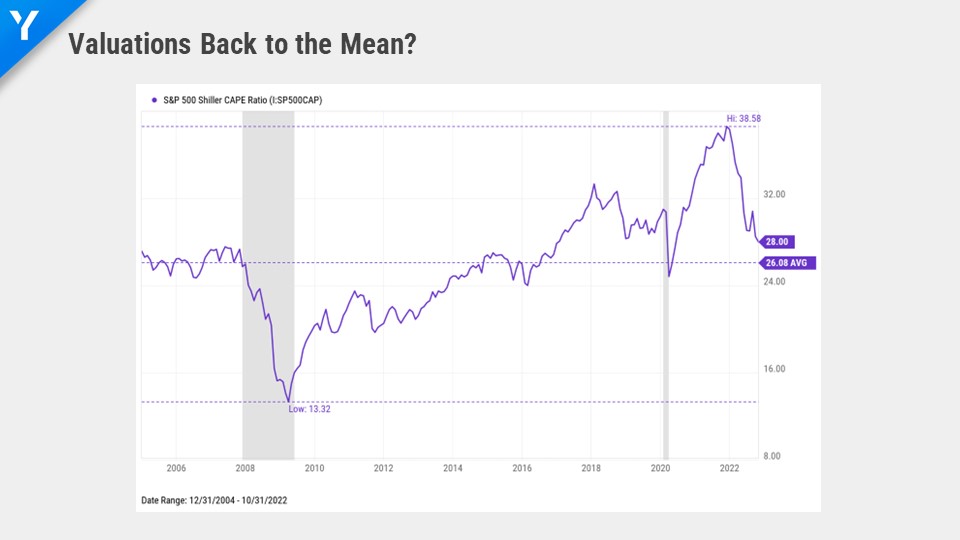

As we assess markets now, we remain cautious on the near-term outlook yet more optimistic about future returns given the reset of interest rates and stock valuations. The weight of the evidence leads us to believe that equity markets have not fully discounted the effects of the Fed’s past and future rate hikes, and their likely effects on earnings. Most of the losses in stocks this year have come purely from valuations contracting. The second leg of the bear market is likely to manifest in an earnings recession, and most forecasts and guidance have offered limited cuts to growth rates in 2023. We have started to see these cuts during the late summer / early third quarter earnings cycle and expect that will continue into next year. With a very likely 75 basis point increase by the Fed in November, another increase in December, and perhaps more in 2023, we expect an earnings trough is some months off, and it is too early to properly discount the depth and length of the contraction.

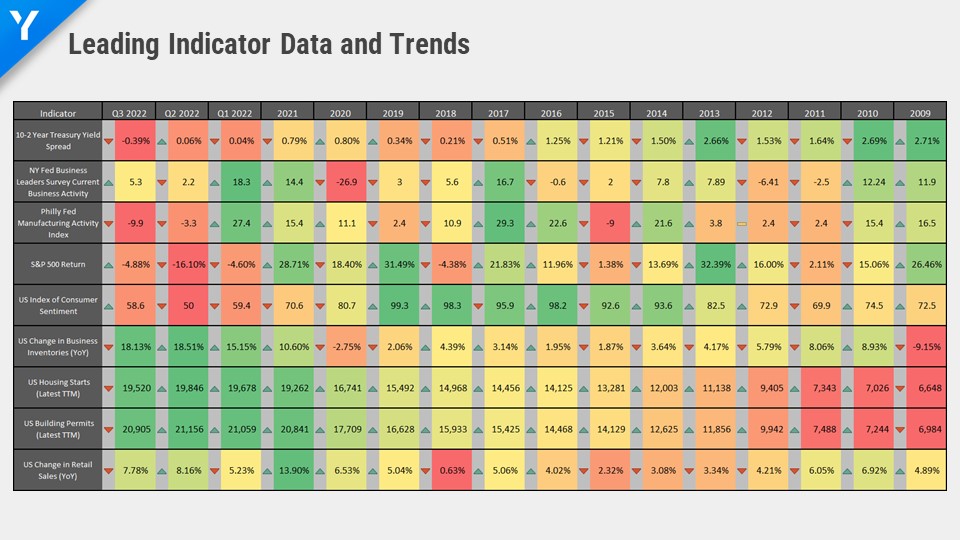

Leading economic indicators have been weakening for several months and monetary conditions and liquidity continue to tighten as the Fed accelerated to its full quantitative tightening program in September. We believe the volatility in the stock, bond and currency markets have been closely correlated to the drop in liquidity and the money supply. Markets have been conditioned for more than a decade of abundant cheap money, and the dramatic reversal of that resource is causing rapid swings in sentiment and positioning.

As the economy likely deteriorates further due to these conditions, we expect that the Fed will eventually pause its rhetoric on rate hikes, but it’s unlikely to happen until 2023. Given their late arrival to the inflation fight, we expect they will err on the side of excess tightening rather than backing away before it is clearly in retreat. Chairman Powell’s Jackson Hole speech was very blunt in its tone after the summer rally where stock investors were predicting (or hoping?) the Fed would pivot quickly and go back to the easy conditions of the past. We are not convinced that markets have fully embraced a new regime of monetary policy and “higher for longer” interest rates.

We continue to favor value-oriented strategies. During the third quarter, all stocks fell but value underperformed for the first time this year, keeping it as cheap (or cheaper) on a relative basis to growth. We added exposure to value and small cap stocks at the end of the second quarter following the June market low. Among U.S. stocks, we see small caps as the area of best opportunity. Many of those stocks now trade below historical norms, while large U.S. stocks are still at above average valuations and more susceptible to earnings declines.

We see excellent long-term opportunity in international markets; in certain sectors, these stocks appear the most attractively valued since the Great Recession 13 years ago. Their slight underperformance to the U.S. in 2022 has primarily been affected by the dollar’s incredible strength more than valuation and earnings. With our value bias, developed international stocks naturally fit that style profile given their lower exposure to technology and traditional growth and high multiple sectors. We think the dollar’s strength has been largely due to the Fed being consistently aggressive in tightening policy, as other countries catch up. As the U.S. economy weakens from policy moves and the late economic cycle, we expect the dollar will peak; if it weakens, that will offer additional upside to international stocks that are already trading at recessionary valuations.

In the bond market, we did not make any changes to our portfolios this quarter following several adjustments during the summer. We added a quality bias by increasing exposure to Treasury and global sovereign debt versus corporate and high yield bonds. As with stocks, international unhedged bonds offer relative value with the dollar trading at multi-decade highs against other currencies.

We did not make any changes to our alternative investment allocation. We continue to see diversification benefits in the managed futures and event driven sectors. We are also realistic about their future relative performance in this bear market. Our current managers have outperformed stocks and bonds by margins between 10-45% just this year! We will consider using some of these funds as a source of new investment in stocks if we see financial conditions improve or valuations become more compelling.

We have often been asked this summer and fall about investment tactics now given the losses in stocks and bonds, and the uncertainties that lie ahead. This has been an exceptionally rare year in that there have been declines in almost every asset class! The silver lining for investors is that future returns for those assets (and cash) will be higher compared to January. For your portfolio, we examine what are tomorrow’s best return opportunities given the risk profile today. Those opportunities may trend from “good” to “very good” to “excellent”, but that doesn’t mean you shouldn’t own some of them when they are “good”. We believe we own the right stocks for tomorrow and aren’t focused on yesterday’s performance. To outperform the market, you generally must take some contrarian position to conventional wisdom. We expect that the 2020’s market will be very different from the 2010’s. We see many other investors and advisors still expecting the “good old days” to return, and frankly we have moved on. For those of us old enough to remember, the 2000’s market did not resemble the 1990’s after the tech stock bubble burst, and the 2010’s did not match the 2000’s after the Great Recession. When a new bull market begins, it will almost certainly not look like the last one.

We balance our optimism with a sense of caution. We don’t think today is the time to call a stock market bottom, get very aggressive in positioning, and add excessive risk. The old saying is still true…”Don’t fight the Fed”. Until we see improvement in financial conditions, we will invest smartly in areas that we believe offer a margin of safety. When we think it’s time to get more aggressive, we will share it in our commentary or send out a note announcing the tactical change.

Thank you for your patience and confidence throughout this difficult year. We are always mindful of the financial challenges and stress that have persisted in 2022. We put considerable thought and perspective into allocating your capital and are deeply humbled by your trust in our company.

Email Signup

"*" indicates required fields

Chattanooga

Union Square Suite 600

Chattanooga, TN 37402

Nashville

3100 West End Ave Suite 860

Nashville, TN 37203

Atlanta

3290 Northside Parkway NW, Suite 850

Atlanta, GA 30327