July 26, 2023

2023 Second Quarter Investment Update

Throw Out the Rulebook

Stocks surged higher in the second quarter, highlighted by the S&P 500 Index technically exiting a bear market in June. Bond prices slipped as the stronger than expected U.S. economy and resilient job market pushed interest rates higher and expectations of Federal Reserve rate cuts out into 2024. Inflation continued to trend lower, but the combination of economic strength and easy seasonal comparisons were warning signs that the Fed still has work to do to achieve its targets.

Corporate earnings posted a slight decline in the first quarter of 2023, the second consecutive quarterly decrease in annual profits, but the overall rate of companies beating sales and earnings estimates was cheered by Wall Street. Expectations had been lowered for many companies late last year, and the stock market was in the mood to reward “better than feared” outcomes. As we head into second quarter earnings season and the rest of 2023, the bar appears higher for many companies to rally on results.

Many investment strategists were caught off guard by the nature of this year’s stock market rally, which confounded the traditional evidence and trends that accompany a new bull market. Following the banking crisis in March, the rally was even more dominated by the largest companies in the U.S. market. This led to a quickly popularized term for these companies; the “Magnificent Seven”, representing the seven highest valued companies by market capitalization (Apple, Microsoft, Alphabet, Amazon, NVIDIA, Tesla, Meta Platforms). Each of these companies returned between 36 to 190% in the first six months of 2023, while the S&P 500 returned “only” 17%.

While there were some fundamentally positive events surrounding these companies, most of their stock gains were driven by higher valuations and investors willing to pay richer prices and accept smaller earnings yields on the expectation of future growth (perhaps combined with fear that other companies would be more impacted by a recession or earnings slowdown). This phenomenon defied one of the usual tenets of an emerging bull market; typically, new sectors and companies tend to lead a recovery. Many of the Magnificent Seven were among the best performers during the 2010’s bull market and continued to expand their performance lead (and valuation) versus the rest of the market.

Their rally also occurred in a period where interest rates remain at much higher levels than during much of the prior bull market. Money market funds are now routinely yielding 5% and cash returns are expected to drift even higher with a Federal Reserve rate hike in July. As a result of the valuation expansion and higher interest rates, the “equity risk premium” (measured as the difference between the earnings yield on the S&P 500 and Treasury bonds) is at its narrowest level since 2007, just before the Great Recession.

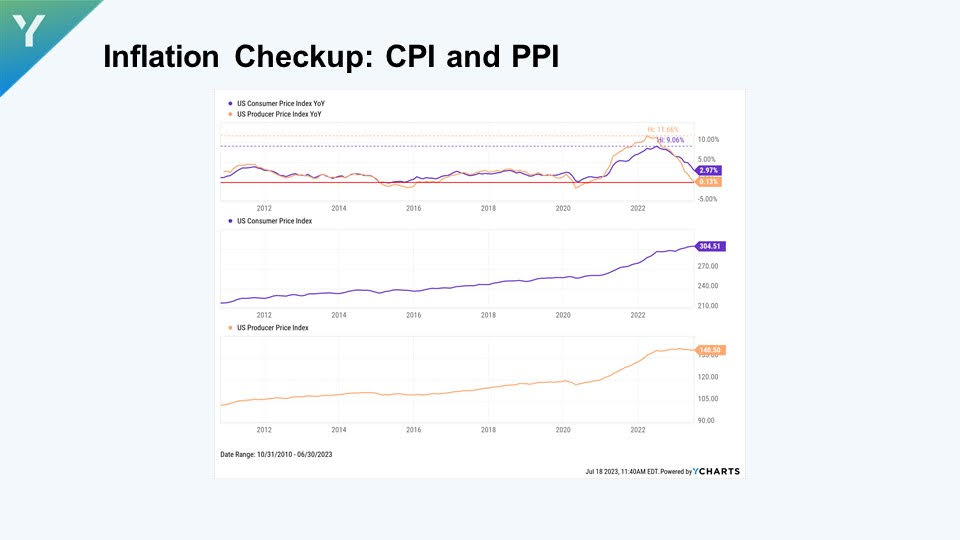

Inflation as measured by the Consumer Price Index ended June at a 3.0% annualized rate, the lowest level since March 2021. Core CPI (ex‐food and energy) remains at 4.8% as of June and Core PCE has been tracking between 4.6‐4.7% over the past several months, well above the Federal Reserve target level of 2%. While consumers and investors can be relieved that inflation has dipped well below peak levels, there remain challenges ahead. The June 2022 CPI measure was 1.2%, the final high result of last year’s cycle. Four of the six measures in the second half of 2022 are between 0 and 0.2%; it’s unlikely annual headline inflation will dip significantly for the rest of 2023, barring an economic shock. If the economy does not weaken and unemployment does not tick significantly higher, the Fed will have little incentive to cut interest rates.

Stocks and Bonds Go Their Separate Ways

Stocks were uniformly and strongly positive in the second quarter, led by the aforementioned Magnificent Seven. A persistent theme during the quarter was the lack of breadth in the rally, which we addressed in last quarter’s outlook. Breadth can be defined as broad participation in gains across different sectors and sized companies in the economy. For much of the second quarter, the rest of the U.S. market’s 2023 return excluding those seven stocks toggled near zero. By June, breadth began to improve slightly, but not in a definitive way that usually accompanies a new bull market.

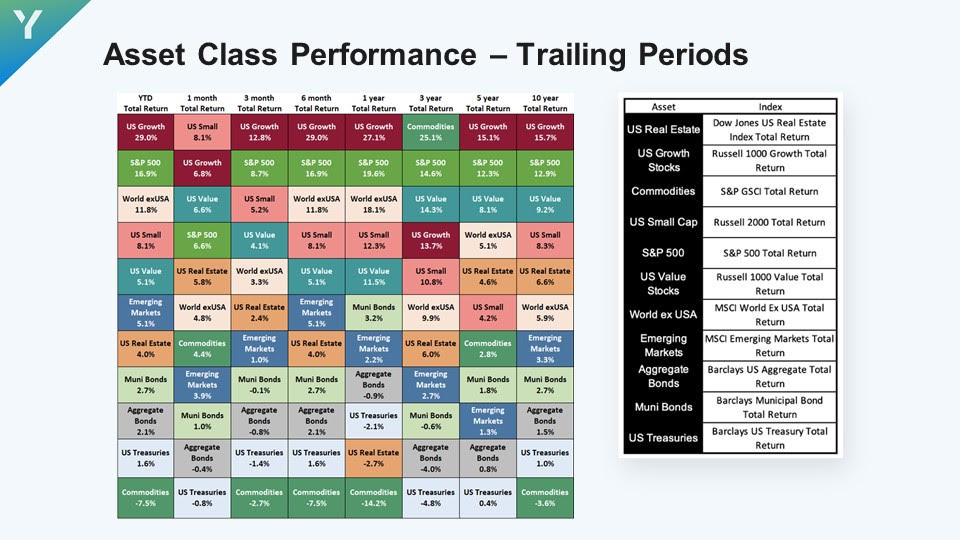

The lack of breadth was again reflected in the difference between market cap performance. Large cap US stocks (as measured by the Russell 1000 Index) were up 8.6%, while small cap US stocks (Russell 2000) were up 5.2%.

International stocks (MSCI EAFE) were up 3.0% and Emerging Markets (MSCI EM) were up 0.9% in the second quarter.

There was again a significant dispersion in returns between growth and value stocks in the second quarter. Large growth stocks were up 12.8% (Russell 1000 Growth) vs. 4.1% for large value (Russell 1000 Value). Among small stocks, the gap was 7.2% for growth (Russell 2000 Growth) vs. 3.2% for value (Russell 2000 Value).

Without any immediate collateral damage from the bank failures in March, the bond market refocused on stronger than expected economic data and yields rose during the second quarter. US taxable bonds (Bloomberg US Aggregate Bond Index) fell ‐0.8% and municipal bonds (Bloomberg Municipal 1‐15 Year Index) were down ‐0.4% for the quarter. Corporate high yield bonds were up 1.8% while international bonds were down 1.5%.

Strategy Update

Our equity strategy returns lagged the broad benchmarks in the second quarter, primarily due to our underexposure to the Magnificent Seven S&P 500 stocks. Our equity strategy was up 5.7% in the second quarter and is now up 10.5% year‐to‐date. The MSCI ACWI global index returned 6.2% for the quarter and is up 13.9% for 2023.

Both our taxable and tax‐free bond strategies again outperformed the benchmark in the second quarter. The taxable strategy slipped only ‐0.3%, outperforming the Bloomberg US Aggregate Index which fell ‐ 0.8%; year‐to‐date, our strategy increased its advantage to a 3.3% gain vs. 2.1% for the Bloomberg Agg.

Our municipal bond focused strategy was down just slightly in the second quarter, ‐0.03% versus the Bloomberg 1‐15 Year Municipal index, which fell ‐0.4%. Year‐to‐date, our municipal strategy is up 2.8% vs. 1.9% for the Bloomberg index.

Our outperformance in both bond strategies was helped primarily by our allocation to high yield and emerging market local currency debt, both of which exceeded the respective benchmarks by wide margins.

Our liquid alternative strategies were positive for the second quarter, up 1.3% in aggregate. Managed futures was the standout sector, up 3.4%, while our event‐driven strategies were down between ‐0.6 to ‐1.1%.

Outlook Update

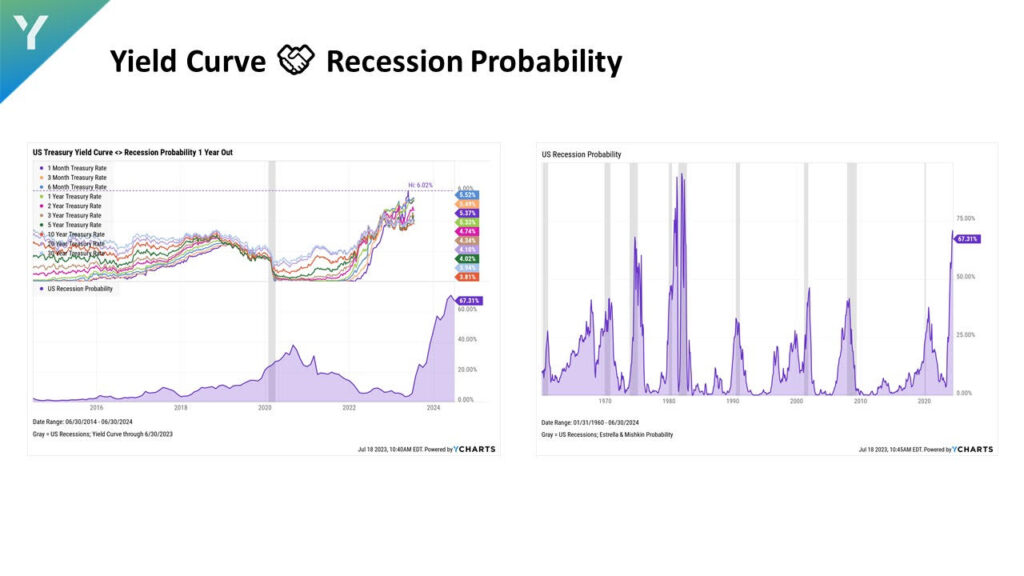

Investors and economists struggle to reconcile the narrative created from the stock market rally in the first half of 2023. While the bond market continues to display an inverted yield curve, forecasting the prospect of lower inflation (but also lower growth), U.S. stocks are trading at historically rich valuations and behaving as if there will be a soft (or no?) landing in the economy in 2024.

We have remained neutral in our portfolio positioning and see a mixed set of variables, but certainly enough concerns that temper our enthusiasm to chase the hottest stocks in this rally.

From a technical, price‐driven evaluation, the market has rallied consistently throughout 2023 without any meaningful correction or pullback. This has been the best, strongest evidence that it is not timely to get defensively positioned. Market breadth did improve in June, but the evidence has not been overwhelming compared with other historical bull markets. As investors, we respect price momentum; to only focus on valuation and fundamentals over the last 15 years, an investor would have missed significant contributors and exposure to the 2009‐2020 bull market.

On almost every other factor, however, stock markets are flashing warning signals that we believe should not be ignored. Fundamentally, the U.S. stock market as measured by the S&P 500 is trading at some of its richest valuations in the last 25 years; in hindsight, it was nowhere near cheap levels at the October low, particularly compared to the 2002, 2009 or even 2020 bear market floors. It was arguably “mildly” overvalued at last year’s low relative to several measures but has now rallied almost 30% from those levels. In fact, with Treasury yields hovering between 4 to 5.5%, the S&P is now arguably more expensive than it was at its January 2022 peak compared to the alternatives of cash and bonds.

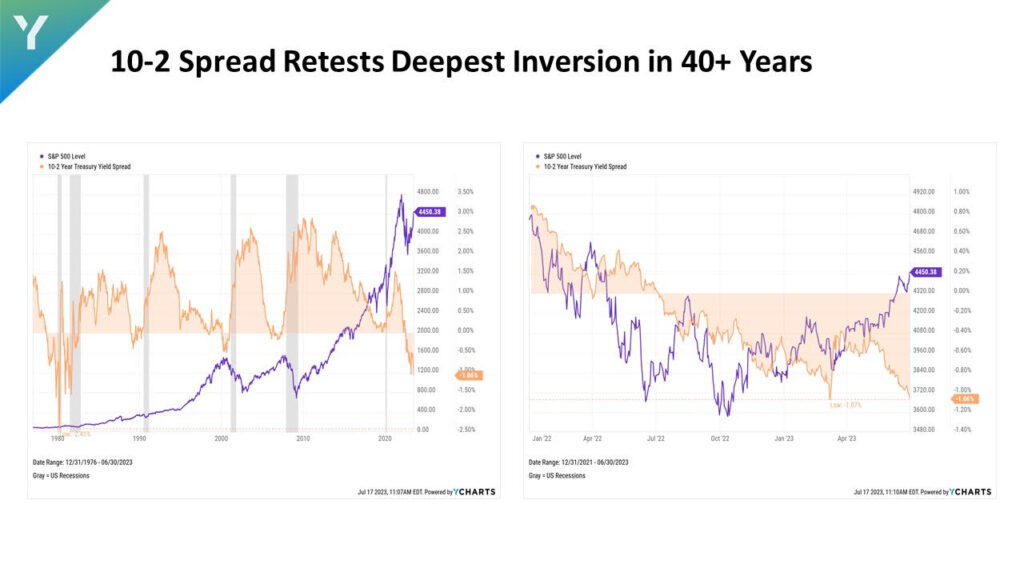

The stock market rally is occurring amid several economic cycle trends that typically forewarn a recession. The yield curve remains deeply inverted; there is over a 1.5% gap between Treasury bill yields and the 10 Year Treasury bond, as the bond market expects enough contraction in growth to necessitate significant rate cuts in the future. The money supply (as measured by M2) has been in contraction for much of the last year and the Fed is continuing their quantitative tightening program of allowing $90 billion of maturing bonds on their balance sheet to be absorbed by the market each month. The balance sheet is now back below levels in March before they created the Bank Term Funding Program in response to the Silicon Valley and Signature Bank failures.

Market sentiment has dramatically shifted this year from cautious to optimistic. The ratio of bull to bear investor positioning, call vs. put option buying, and the VIX index are all flashing high degrees of complacency. Even though rate cuts are priced out into next year, the mainstream narrative is now there will be a soft landing for the U.S. economy. In this scenario, corporate earnings growth accelerates into the end of 2023 and 2024, yet the Federal Reserve is satisfied with declining inflation that they will aggressively cut rates next year.

It is difficult to square both outcomes. If the economy is resilient enough to deliver strong profits, the Fed is unlikely to cut rates to the depth the market expects. If the Fed is forced to react to the other half of their mandate (full employment over stable prices/inflation), it likely means the economy has hit a speed bump and the outlook for the market’s implied 10% earnings growth in 2024 is murky at best.

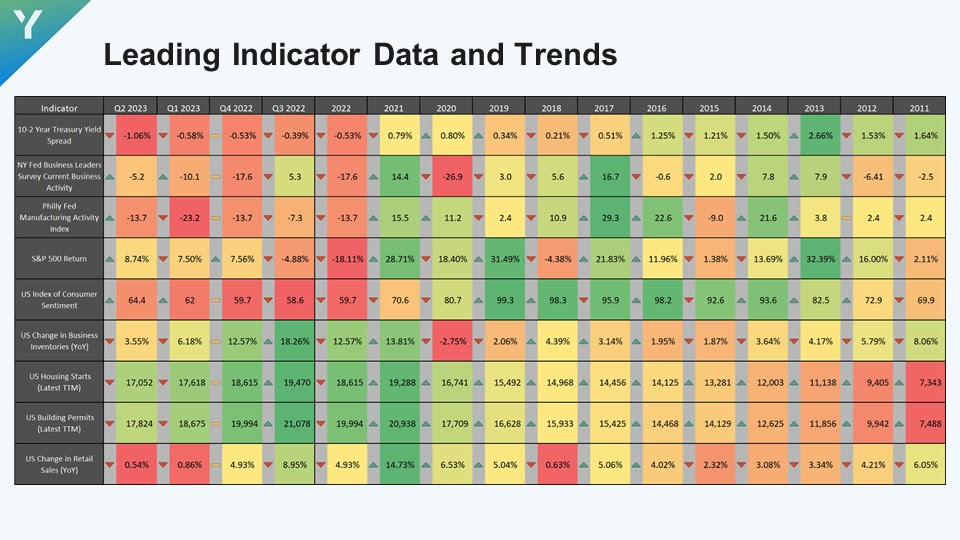

Reviewing economic conditions, our expectation for recession has been delayed, not canceled. There are few signs the economy reaccelerated in the second quarter, other than consumer confidence. And this measure tends to track current conditions – if a consumer is employed and their financials are better (e.g., their investment portfolio is up), they tend to report better survey results. As a predictive measure, many of the other leading indicators tend to be more accurate forecasts of future economic activity.

We did not make any tactical adjustments to our portfolios following the changes at the beginning of the second quarter. At that time, we reduced our exposure to large cap growth stocks via S&P 500 index positions and added exposure to smaller, multi‐cap stocks with a bias toward value and profitability. As the market broadened out from the Magnificent Seven stocks late in the second quarter, our portfolios began to benefit from this trend change.

We are maintaining our allocation to international and emerging market stocks; Japan has been a particular standout performer in 2023 due to its economy finally showing signs of inflation, improved economic growth, and the potential for central bank policy change for the first time in decades. Emerging markets have benefited from currency appreciation versus the dollar this year; this tends to auger well for future returns as their debt markets show signs of stability and increased capital flows.

In bond portfolios, we reduced high yield and increased exposure to high quality fixed income early in the second quarter. While the riskier high yield bonds continue to perform well, we see them as now mirroring many of the risks in the stock market. With the yield premium on these bonds narrow relative to high quality bonds, we see benefit in moving to safer, more predictable returns. An investor can find 5‐6% yields with little risk in the current bond market and we do not see an advantage in pursuing richer yields with economic clouds on the horizon.

We are maintaining our current alternative investment allocation. Our managed futures position has shown an ability to benefit from shocks in the market; it also benefits from the rise in cash yields in their underlying Treasury portfolios. With a very complacent market and subdued volatility, we think a more defensive position is warranted to guard against the unexpected next worry for the stock market.

The current economic cycle continues to defy norms and rewrite how economists and market strategists interpret data and events. Perhaps the best explanation for this phenomenon is the massive fiscal stimulus and deficit spending regime that persists to this day from the pandemic. In many ways, the U.S. $1.5 trillion current annual deficit can distort the economic cycle and disguise weaknesses and declines that might have already emerged in other eras. There has been a high correlation between government spending and corporate profit margins; with budget deficits still approaching 7%+ of GDP (which only occurred between 2009‐2011 and 2020‐2021 since World War II), it may allow the economy to delay a classic recession and business cycle.

It is our expectation there is no economic “free lunch” where we simply skip a business cycle and move to a new expansion – there are plenty of signs that challenges lie ahead, many of which could appear in months rather than years. Combined with stock valuations in the top decile historically, we do not see a long runway that accompanies a new multi‐year bull market. In 2009 and 2020, the stock market started at much cheaper levels and was in the early stages of multi‐year government spending programs and support from central banks. Today, we are in the latter phase of pandemic stimulus, central banks are neutral at best in their fight against inflation, and there are few catalysts for the economy to pick up momentum. The unemployment rate and jobless claims are trending higher, not lower; consumers and corporations are refinancing higher levels of debt at higher rates each month, and investors are encouraged to be cautious and demand higher returns with 5% risk‐free yield courtesy of Treasury bills.

Despite these dour forecasts, the good news for investors is we are now in a TARA (“There Are Reasonable Alternatives”) world rather than TINA (“There Are No Alternatives”) world when it comes to stock investing to make reasonable returns. We encourage investors to consider bonds, alternative investments and cash in their portfolios for diversification purposes where appropriate. We also advise being selective in stock sector exposure and tactical in deploying cash into stocks now. As an investor, the best roadmap for excellent returns is to be contrarian to the crowd. When buzzwords like “AI” dominate financial media without any quantitative or financial metrics behind them, it should give you pause that speculative bubbles exist in the market. Our investment managers tend to focus on price, profitability and consistency, not hype. At the same time, we are indeed looking for the next generation of companies that could be the Magnificent Seven of 2033 or 2043 – remarkably, of the top 10 stocks in the S&P 500 in 2003, only one of them, Microsoft, outperformed that index over the subsequent 20 years. By focusing on smaller companies, we plan to invest in stocks that have a long runway for growth no matter what the economic “landing” and are positioned to provide returns that meet your objectives.

Thank you for your confidence in our stewardship of your and your family’s wealth. Please contact any of our advisors if you would like to discuss how these ideas may apply to your investment strategy and financial plan.

Email Signup

"*" indicates required fields

Chattanooga

Union Square Suite 600

Chattanooga, TN 37402

Nashville

3100 West End Ave Suite 860

Nashville, TN 37203

Atlanta

3290 Northside Parkway NW, Suite 850

Atlanta, GA 30327